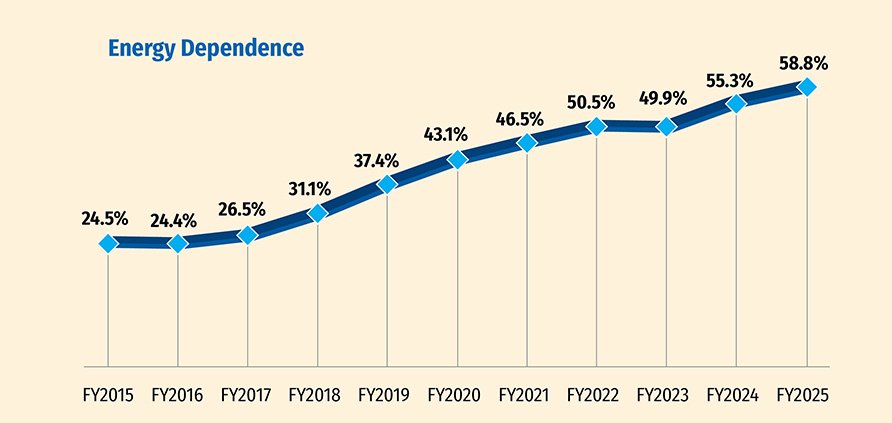

With a high energy import dependency of 59%, Bangladesh is being severely affected by the Middle East war due to the disruption of its energy supply chain. Energy dependency has risen sharply over the past 10 years from 25% in 2015 to 59% in 2025. In the past, Bangladesh was less impacted by the global energy crisis because we were less dependent on fuel imports. We faced huge load shedding in the past, not due to a primary fuel supply shortage, but because capacity addition lagged behind power demand growth. The situation has changed as energy dependency rises constantly. In early 2022, at the beginning of the Ukraine war, a global energy crisis was created, and we were severely affected due to abnormally high primary fuel import prices.Since 2022, we have been facing load shedding not due to capacity shortage but due to fuel supply shortages. As our energy dependency has increased over the past decade, we have become increasingly vulnerable to global crises.

Situation before Present Crisis: We were in crisis even before the Iran war, primarily due to a domestic natural gas supply shortage. In FY 2015, domestic natural gas contributed 73% of TPES (Total Primary Energy Supply), but in FY 2025, it came down to only 37%. Even LNG import of 6.75 Mtoe helped only raise natural gas contribution to nearly 53%. We have observed a lot of uncertainties in offshore drilling. LNG imports faced limitations due to the failure to implement the 4th and 5th FSRU projects. Additionally, the utilization of the existing two FSRUs remained below full capacity, operating at only 77% in FY 2025 and 68% in FY 2024. Industries have been the worst victims of this crisis. The power sector has been operating only about half of its 11,000 MW capacity from gas-based power plants. Consequently, BPDB is forced to operate costly HFO-based power plants, causing the cost of electricity supply to skyrocket. However, the cooking and transport sectors remained relatively stable, with less impact, before the outbreak of the Middle East war.

Impact of Middle-East War: Since the start of the war, we have been facing strain across all sectors. At the beginning of April 2026, summer heat and high humidity had begun to severely impact the electricity sector. Furthermore, a substantial increase in LPG prices for cooking is causing households to switch to electric induction or infrared cookers, putting added pressure on the electricity supply. Industry has been facing a natural gas crisis, and now, in addition, increased load shedding may interrupt further production. Meanwhile, the impact of the present fuel supply crisis on the transport sector has made headlines globally.

Petrol and Octane Availability: For the first time in many years, the transport sector is facing an energy crisis. There might definitely be disruptions in the supply of major fuels, such as petrol, octane, diesel, marine fuel (for ocean-going vessels), and Jet A-1 (for aviation), due to the interruption of shipping movement through the Strait of Hormuz. The long queues of cars and bikes for petrol and octane are unprecedented, driven primarily by panic buying, even though about 70% of these fuels are produced locally. Public and private sector fractionation plants process Condensate, NGL (Natural Gas Liquids) from gas fields to produce octane, petrol, diesel, kerosene, LPG, and other petroleum products. For example, in FY 2024, demand for petrol and octane was 430,836 and 385,435 metric tonnes, respectively (total demand 816,271 tonnes), while local supply was 270,440 and 263,959 tonnes, respectively (total local production 534,400 tonnes). Local production contributed about 66% of total octane and petrol demand. ERL (Eastern Refinery Limited) produced 41,775 tonnes from imported crude oil (covering 5% of total demand), while direct import was 259,790 tonnes (32% of total demand, though only 29% consumed, with the rest added to stock). With local production, supply from ERL, and available stock, there should not be a crisis like this, even if there are no octane and petrol imports for two or three months.

Diesel Supply is of Major Concern: The availability of diesel should be our main concern, as almost two-thirds of total final oil consumption is diesel. Transport and agriculture, two major sectors, are heavily dependent on diesel. These two sectors consume almost 85% (transport 65% and agriculture 20%) of total diesel consumption. For example, in FY 2024, diesel consumption was 42.5 lakh tonnes, which is 63% of the total oil demand (67.6 lakh tonnes, excluding LPG imports by the private sector and HFO imports by IPPs).To meet the 42.5 lakh tonnes of diesel demand, local supply from indigenous sources was only about 1.5 lakh tonnes (3.5%), while ERL supplied 5.8 lakh tonnes (13.6%). The remaining 35.3 lakh tonnes (83% of the total demand) was imported. Therefore, diesel import dependency is huge, necessitating careful planning for a continuous supply from diversified sources.

Price Volatility: Prices of most major fuels have gone crazy within a month of the outbreak of the Iran war. The LNG spot price in the Japan-Korea market has almost doubled from roughly $10/MMBtu to $20/MMBtu. Brent crude oil prices have surged by nearly 50%, which directly impacts the LNG prices in our long-term contracts. Arabian Light crude is priced similarly to Brent, while Murban crude is slightly costlier than Arabian Light.Thermal Coal prices for shipments out of Australia (Newcastle Port) have surged nearly 20%. Coal prices for power plants in Bangladesh are linked to the Newcastle and Indonesian HBA benchmark prices. Prices of refined petroleum products are soaring. A recent newspaper report reveals the import-adjusted cost of diesel has reached nearly 200 Tk/Liter, while the retail selling price is maintained at 150 Tk/Liter. The only exception is the uranium (U3O8 Ore) price, which remains relatively stable during this turmoil, hovering around $85 per pound.

Critical Issue: We have no alternative but to strictly maintain effective austerity measures until the crisis fully resolves. The government should adjust fuel prices as soon as possible, not only to avoid a financial crisis but also to bring discipline to the energy market. For example, the BERC set the LPG price for April 2026 at Taka 1940 per 12kg cylinder, aligned with the global price, which is nearly 30% jump from the previous month. However, there is no market chaos regarding LPG availability and no financial burden on the national exchequer. While the decision to adjust fuel prices may be unpopular now, it can prevent more unpopular decisions in the future.

Md. Mizanur Rahman, Former Member, Bangladesh Energy Regulatory Commission (BERC)

Download Special Report As PDF/userfiles/EP_23_22_Special_Article.pdf