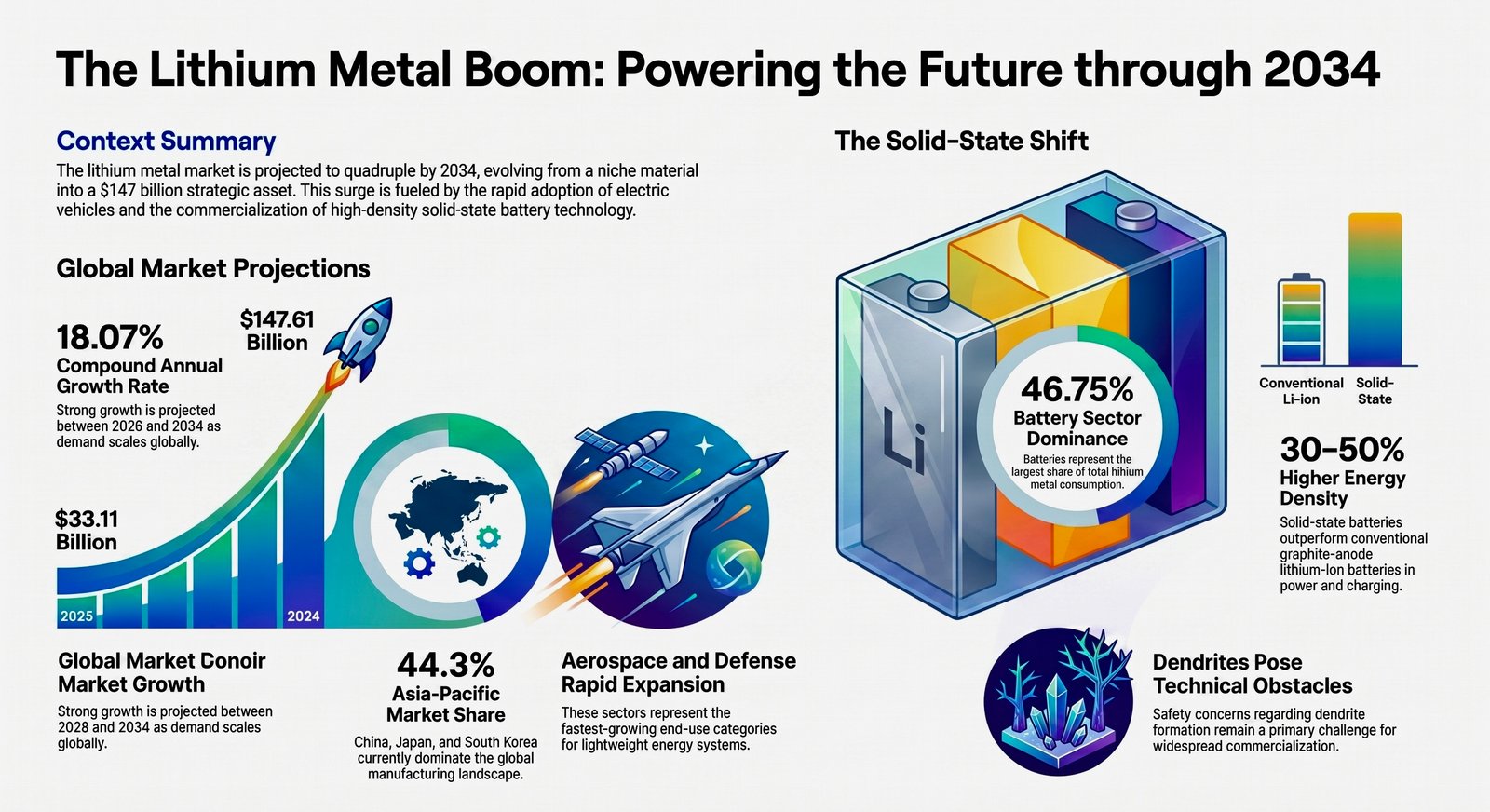

The global lithium metal market is expected to witness remarkable growth over the next decade, driven by soaring demand from electric vehicles (EVs), renewable energy storage systems, and next-generation battery technologies. According to the latest report by Polaris Market Research, the market is projected to grow from USD 33.11 billion in 2025 to USD 147.61 billion by 2034, registering a strong compound annual growth rate (CAGR) of 18.07% during 2026-2034.

Lithium metal, the pure metallic form of lithium, is emerging as a strategic material for advanced batteries due to its exceptional energy density. Unlike lithium carbonate or lithium hydroxide, which are used as intermediate materials, lithium metal is increasingly being adopted as the preferred anode material for solid-state and lithium-sulfur batteries, enabling higher energy density, faster charging, and improved battery performance.

EV Growth Drives Market Expansion

The rapid expansion of the electric vehicle industry remains the primary driver of lithium metal demand. Global EV sales exceeded 17 million units in 2024, marking a 25 percent increase over the previous year. As automakers accelerate the development of batteries with higher performance than conventional graphite-anode lithium-ion batteries, lithium metal has become a key material for future battery technologies.

The market is also benefiting from growing investments in renewable energy. With renewable sources accounting for around 32 percent of global electricity generation in 2024, and expected to rise significantly by 2030, demand for efficient energy storage solutions is increasing. Lithium metal batteries are considered well-suited for large-scale energy storage because of their superior efficiency and energy retention capabilities.

Solid-State Batteries Offer Major Opportunity

The report identifies solid-state batteries as the most significant growth opportunity for the lithium metal industry. These batteries promise greater safety, higher energy density and longer operational life compared to conventional lithium-ion batteries.

Commercial development is gathering pace. In 2025, Tailan New Energy introduced an AI-enabled smart solid-state battery featuring integrated sensor technology. In March 2026, POSCO Future M partnered with Kumho Petrochemical and BEI to develop anode-free lithium-metal batteries capable of delivering 30-50 percent higher energy density and significantly faster charging.

Industry analysts believe continued advances in battery-grade lithium purity, localized refining capacity and recycling infrastructure will further accelerate market growth.

Batteries Dominate End-Use Demand

The battery sector accounts for nearly 46.75 percent of total lithium metal consumption, making it the largest end-use industry. Lithium-ion anode materials and next-generation battery applications represent around 42.6 percent of overall demand.

While hard-rock lithium deposits currently supply the largest share of raw materials, recycled lithium is emerging as the fastest-growing source as manufacturers seek greater supply security and sustainability.

Beyond batteries, demand is also increasing from specialty chemicals, pharmaceuticals, aerospace and defense industries. Aerospace and defense are expected to record the fastest growth among end-use sectors due to increasing requirements for lightweight, high-performance energy systems.

Asia-Pacific Leads Global Market

Asia-Pacific dominates the global lithium metal market with an estimated 44.3 percent share, supported by China’s extensive battery manufacturing industry and integrated supply chains across Japan and South Korea.

North America is strengthening its position through investments in domestic battery manufacturing and critical mineral supply chains. Europe is also expanding rapidly, supported by stricter battery recycling regulations and growing investment in advanced battery technologies.

Meanwhile, Latin America and the Middle East and Africa are expected to play increasingly important roles as suppliers of lithium resources and processing capacity.

Supply Risks and Safety Challenges Remain

Despite its strong outlook, the lithium metal industry continues to face significant challenges. Safety concerns related to dendrite formation during battery operation remain a major technical obstacle to widespread commercialization. In addition, lithium production remains concentrated in a limited number of countries, exposing manufacturers to supply chain disruptions and price volatility.

Achieving battery-grade purity at commercial scale also remains technologically demanding and could constrain future production capacity.

Outlook

With electric vehicles, renewable energy storage, aerospace applications and solid-state batteries driving demand, the global lithium metal market is expected to expand rapidly throughout the coming decade. Industry experts believe companies involved in lithium mining, refining, battery manufacturing and recycling will play a critical role in supporting the global transition toward cleaner energy and advanced electrification technologies.