Brent Wanner, Head of Power Sector Unit, Max Schoenfisch, Power Sector Modeller & Hans-Kristian Ringkjøb, Analyst consultant

As the result of falling costs and greater flexibility needs, battery storage is playing a growing role in power systems worldwide, acting as a “multi-tool” that can provide a range of critical system services at once. According to the latest data, the deployment of batteries expanded strongly in 2025 and broadened across markets – with rapid growth in countries such as Australia and Saudi Arabia, where storage is increasingly being used to support the integration of rising shares of variable renewables.

In regions that have been at the forefront of renewable integration and battery deployment, batteries now play an essential role in continuously balancing electricity demand and supply. Comparatively short construction and development timelines are further supporting the rapid deployment of utility-scale batteries in particular: in many markets, projects typically take around two years to develop and commission, giving them an important advantage in systems that seek flexible capacity quickly.

Looking ahead, battery storage deployment is on track to continue accelerating. However, tackling notable barriers, such as regulatory uncertainty and delays in grid connection and permitting, will be key to setting the pace of growth.

Growth in battery storage capacity broke records again in 2025, with new markets growing fast

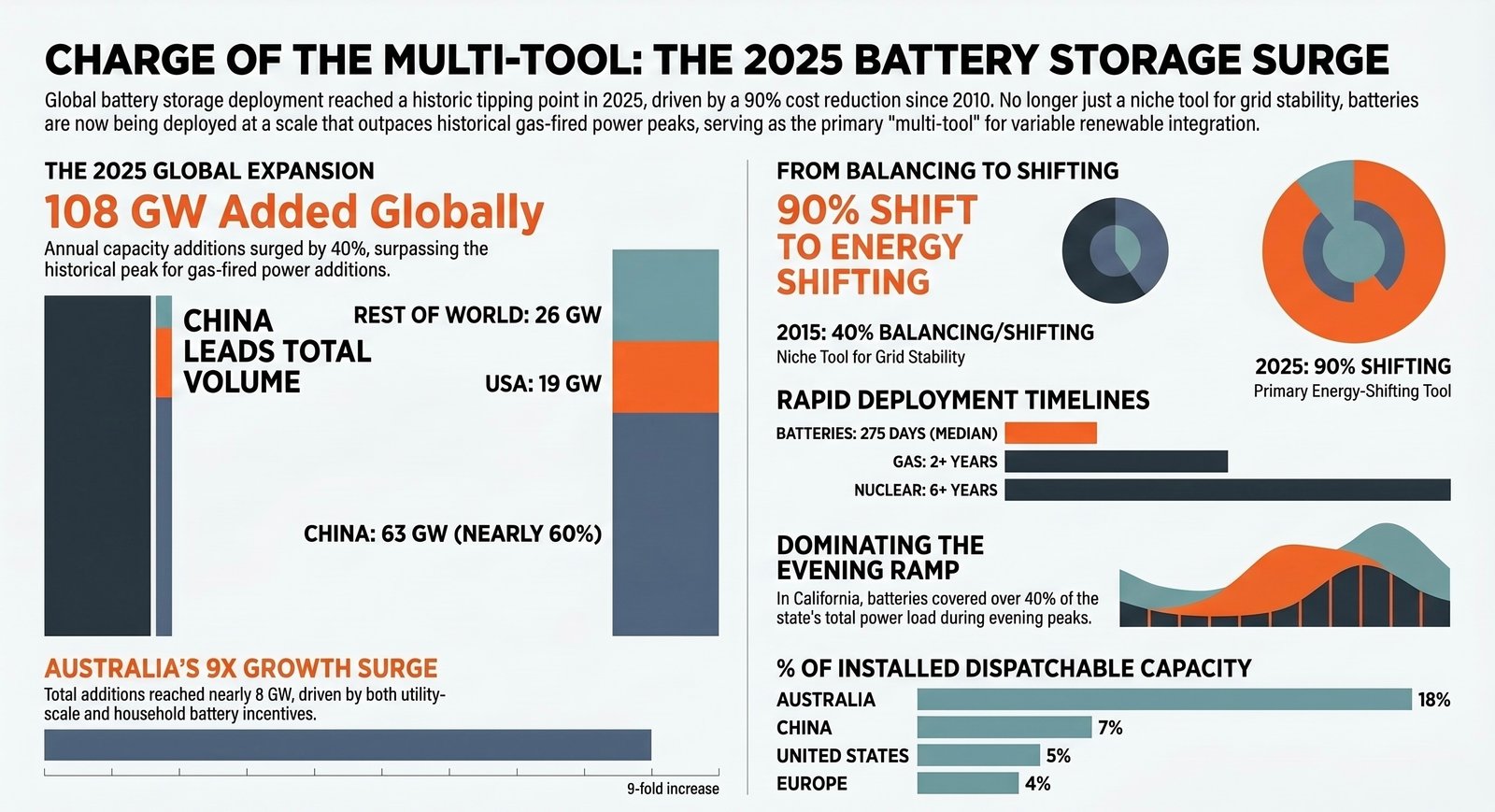

Global battery storage deployment expanded strongly last year. Total capacity additions reached 108 gigawatts (GW), up around 40% from 2024. Annual growth of this scale exceeds the historical peak for gas?fired power capacity additions, which was around 107 GW in 2002.

Utility?scale battery storage accounted for around 87 GW of global battery capacity additions in 2025, around four-fifths of the total. Behind-the-meter battery storage deployment also accelerated, particularly in markets with high retail electricity prices and supportive regulatory and policy frameworks. Around 24 GW of utility-scale battery storage additions in 2025 were co-located directly with renewables, on par with the previous year. This meant the share of capacity co-located with renewables fell just below 30%, as market reforms in China in early 2025 removed broad co-location mandates.

Meanwhile, the rollout of battery storage accelerated across several markets in 2025, pointing to a broadening of global deployment. Australia stood out, with additions surging to nearly 8 GW, almost nine times higher than the previous year. Utility-scale installations in the country rose from under 1 GW in 2024 to around 4.2 GW in 2025, while behind-the-meter additions increased from roughly 0.2 GW to about 3.4 GW, supported by state- and federal-level incentives. In the Middle East, additions topped 3 GW in 2025, more than three times their 2024 level. This was driven almost entirely by Saudi Arabia, where battery storage has become a key source of system flexibility amid a rapidly expanding pipeline of large-scale projects. In Chile, additions approached 1 GW as utility-scale batteries are deployed to absorb surplus solar generation and meet peak demand.

Battery storage now accounts for around 18% of installed dispatchable capacity in Australia, compared with 7% in China, 5% in the United States and 4% in Europe – underlining how rapidly batteries are becoming an important part of the electricity systems in some regions.

In absolute terms, deployment continued to be led by China, the United States and Europe. China added just over 63 GW of battery capacity in 2025, around one-third more than in 2024. Utility-scale installations accounted for around 55 GW of this total, while behind-the-meter additions reached about 8 GW, continuing to steadily expand alongside distributed solar. The United States added 19 GW of battery capacity in 2025 – resulting in year-on-year growth of around 60%, with utility-scale batteries accounting for over 16 GW and behind-the-meter additions rising to nearly 3 GW. In Europe, total battery additions were slightly lower than in 2024 at around 6.2 GW, but with a clear structural shift towards utility-scale systems, where additions more than doubled to about 4.6 GW.

Energy shifting is becoming a key driver of battery storage growth

Supported by a dramatic fall in costs – which declined by more than 90% between 2010 and 2025, driven by innovation, competition and economies of scale – batteries are becoming a key source of short-term flexibility in power systems with rising shares of variable renewables. In this respect, they are highly versatile, capable of providing a diverse range of services that support grid functioning while helping to shift power loads, ensure sufficient capacity and manage congestion.

Early battery projects were concentrated in lucrative but relatively shallow ancillary service markets, which involve the use of batteries to help balance and stabilise electricity grids. But energy shifting – or the ability to store large volumes of energy that can be deployed at a later time – has since become the dominant application: its share of new projects increased from around 40% in 2015 to more than 90% in 2025. Over the same period, the share of projects primarily targeting ancillary services fell from around 45% to about 7%, even as the absolute volume of such projects continued to grow. Batteries are therefore increasingly being used to shift larger volumes of power across the day, while still providing fast-response balancing services to electricity systems as needed. A growing number of battery projects now combine multiple revenue streams and system services, which is reflected in how projects are designed.

As deployment pivots towards energy shifting and renewables integration, the duration of utility-scale batteries is increasing, with a rising share of projects offering four hours of storage or more. In 2025, the average duration of projects commissioned rose to three hours from around two hours in 2023.

Fast delivery times are supporting rapid deployment

Another factor supporting the deployment of battery storage is that it is modular and requires relatively limited onsite infrastructure, which allows projects, in principle, to be built in less than a year. Median construction times are around 275 days for utility-scale batteries – close to solar PV, at about 220 days, but far below gas at over two years and nuclear at more than six years.

Total time to market is often determined less by construction than by permitting, financing and grid connection. In Europe, the United States and Japan, battery projects typically take around two to two-and-a-half years to become operational, while timelines are shorter in China and parts of the Middle East. Nevertheless, batteries can still be deployed more quickly than competing options for boosting system flexibility, such as pumped hydro or gas-fired power plants – giving them a competitive advantage in systems that require additional flexibility within short timeframes.

Batteries are playing a bigger role in balancing electricity demand and supply

As battery deployment has scaled and the duration of batteries has extended, it is changing how the technology interacts with broader electricity system operations, particularly in systems with higher solar and wind penetration. By charging during periods of surplus generation and discharging during periods when demand increases rapidly, batteries are progressively taking on a greater share of short?term ramping and balancing needs.

Some of the clearest examples of this can be found in the United States. In California, solar capacity has grown to over 55 GW. This is greater than the state’s peak load and means that on sunny days, its net load is close to zero – and at times even below it. At the same time, California’s battery capacity has grown from less than 1 GW in 2019 to over 17 GW today. As a result, batteries have been able to discharge more power than ever before – at one point covering more than 40% of the state’s power load on the evening of 29 March 2026, for example. At the same time, batteries are increasingly helping to balance power systems: in the last five years, battery storage has gone from contributing less than 1% of hour-to-hour ramping needs to above 60% in the first quarter of 2026. A similar pattern has emerged in recent years in Texas; in April, batteries contributed to more than 40% of ramping in the ERCOT market.

In South Australia, where wind and solar penetration is among the highest in the world, batteries already provide a prominent share of ramping needs. As one of the earliest movers in large?scale battery deployment, the region saw batteries contribute more than 30% of hourly ramping in February and March.

In Great Britain, where wind is the primary driver of changes in net load, batteries are expanding their role within an increasingly diversified power mix, complementing gas?fired generation, hydropower and increased electricity trade. They are also playing a growing role in the region’s balancing mechanism, where speed is particularly valuable for meeting short?term ramping needs.

Removing barriers could further accelerate deployment

While momentum in battery storage deployment continues to build, some remaining barriers could still slow further progress. Regulatory frameworks play a central role in shaping deployment in both regulated and liberalized power systems. Grid connection and permitting remain key bottlenecks, with non?construction phases often accounting for more than half of total timelines. At the same time, while safety risks remain low relative to the scale of deployment, maintaining public confidence through robust safety standards, transparent communication and active stakeholder engagement is essential.

To unlock the full potential of battery storage, policymakers and regulators need to ensure that regulatory systems recognize the full value of the services the technology offers, while enabling market access and establishing price signals that accurately reflect its various contributions.