GSM Shamsuzzoha (Nasim)

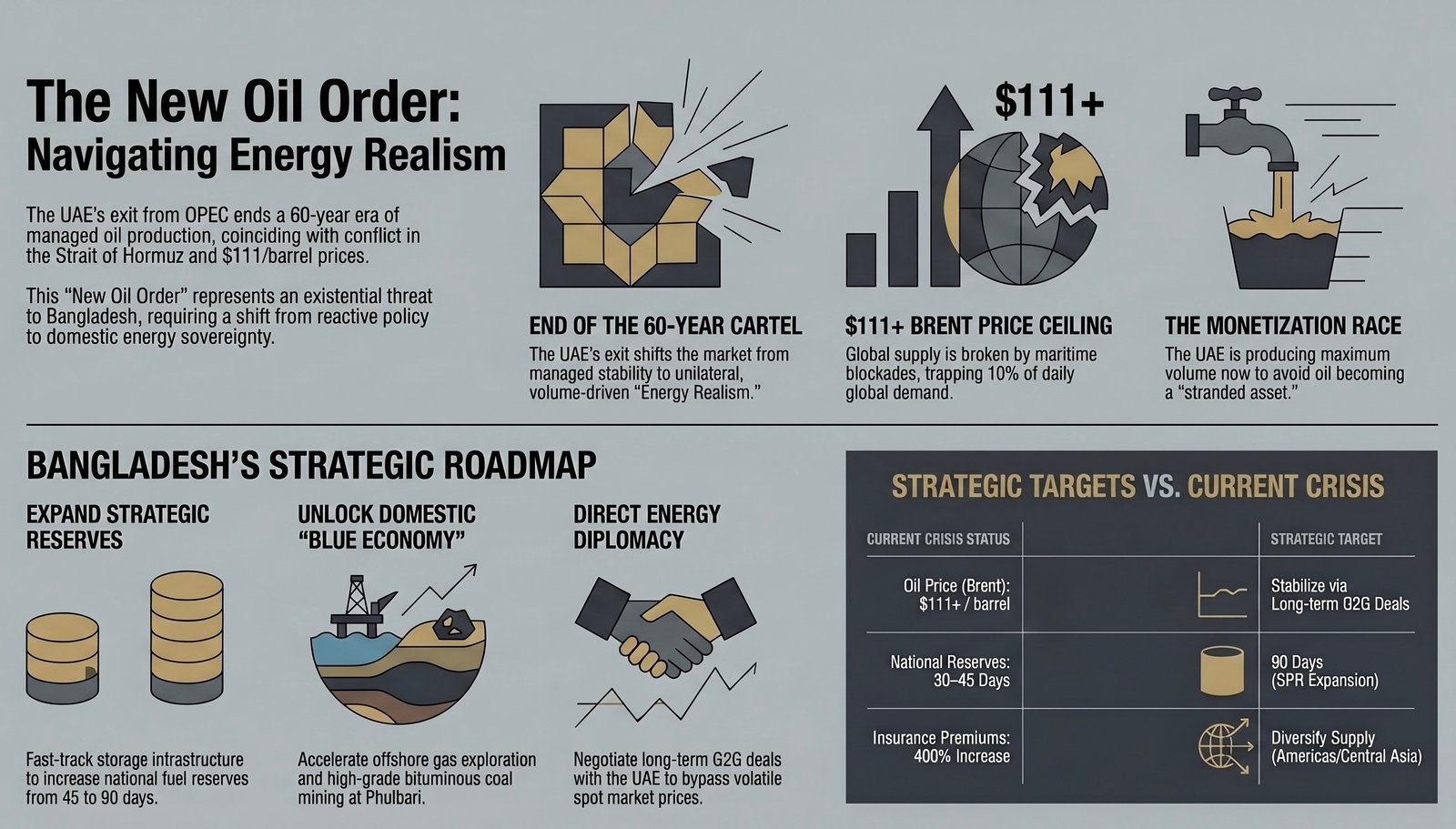

This year’s May Day had been etched into economic history as the day the ‘Old Oil Order’ finally fractured. The formal withdrawal of the United Arab Emirates (UAE) from the Organization of the Petroleum Exporting Countries (OPEC) is not merely a diplomatic reorganization; it is a structural break that ends a sixty-year era of coordinated production.

This exit arrives at a moment of maximum global peril. With Brent crude surging past $111 per barrel and the Strait of Hormuz, the world’s most vital energy artery, choked by the flames of an active US-Israil-Iran conflict, the global energy market is no longer just volatile; it is broken. For energy-import-dependent nations like Bangladesh, this represents an existential threat to macro-economic stability, industrial productivity, and social cohesion.

As per the Guardian, the global oil supply chain was already under severe stress before the UAE’s exit. The war involving Iran has effectively disrupted the Strait of Hormuz, through which nearly one-fifth of global oil flows under normal conditions.

Earlier the Reuters reports:

• Up to 10 million barrels per day disrupted due to maritime blockades and conflict risks.

• Brent crude crossing $110–$111 per barrel, with projections rising further.

In such a constrained system, the departure of the UAE, OPEC’s third-largest producer, introduces a new layer of uncertainty, says the Axios.

Why Abu Dhabi Broke Ranks?

For decades, the UAE was the loyal lieutenant to Saudi Arabia within OPEC. However, the seeds of this exit were disseminated years ago in the boardrooms of the ADNOC (Abu Dhabi National Oil Company). The UAE’s departure is driven by three fundamental misalignments with the cartel:

A. The Monetization Race

Abu Dhabi has invested over $150 billion to expand its production capacity to 5 million barrels per day (mbpd). Under OPEC’s restrictive quota system, nearly 1.5 to 2 million barrels of that capacity sat idle to prop up prices for other, less efficient members. In a world rapidly pivoting toward a ‘Green Transition,’ the UAE leadership reached a cold realization: oil in the ground is a stranded asset. Their new strategy is to ‘produce maximum volume at maximum price’ while the window of global demand remains open.

B. Divergent National Visions

While Saudi Arabia remains focused on high prices to fund its ‘Vision 2030’ projects, the UAE has pivoted toward becoming a global logistics and technology hub. High oil prices, while good for the treasury, threaten the global trade flows that sustain Dubai and Jebel Ali. By exiting OPEC, the UAE regains the sovereignty to calibrate its production to its own economic cycle rather than depending on Riyadh.

C. Collapse of the ‘Central Bank of Oil’

OPEC’s traditional role as the world’s ‘central bank for oil’ required members to sacrifice national gain for market stability. With the rise of U.S. shale and the fragmentation of the OPEC+ alliance (including Russia), the UAE saw the cartel’s influence waning. To Abu Dhabi, paying the ‘membership fee’ of restricted production for a diminishing return on influence no longer made sense.

The UAE’s exit is occurring against the backdrop of a ‘Hot War’ in the Persian Gulf. The conflict involving Iran has effectively turned the Strait of Hormuz into a maritime graveyard.

Current market data from Reuters and The Guardian paints a grim picture:

-

10 Million Barrels Disrupted: Roughly 10% of global daily demand is currently trapped behind maritime blockades or lost to conflict-related shutdowns.

-

The Insurance Trap: War-risk insurance premiums for tankers have increased by 400% in the last 60 days. Even if oil is available, the cost of moving it has become prohibitive for many smaller nations.

-

The ‘Hormuz Chokepoint’: While the UAE has the Habshan–Fujairah pipeline capable of bypassing the Strait, its capacity (1.5m bpd) is insufficient to replace the massive volumes normally flowing through the water.

Historically, an OPEC meeting could calm the markets. Today, the ‘fragmentation of supply coordination’ means there is no 911 for the energy market. As the UAE moves toward a unilateral production strategy, the market loses the ‘buffer’ of spare capacity. We have moved from a ‘managed market’ to a ‘free-for-all’, where price discovery is driven by fear rather than fundamentals.

The Bangladesh Context: A Nation on the Edge

For Bangladesh, the ‘New Oil Order’ is a direct assault on the nation’s aspirations. As a country that imports nearly all of its liquid fuel and a significant portion of its LNG, the $111/barrel price point is a fiscal wrecking ball.

Bangladesh’s foreign exchange reserves have been under sustained pressure since the post-pandemic recovery. With oil prices crossing the $110 threshold, the monthly import bill for the Bangladesh Petroleum Corporation (BPC) is projected to double.

-

The LC Crisis: Commercial banks in Dhaka are already struggling to open Letters of Credit (LCs) for essential commodities. An oil-driven dollar drain will starve other sectors, such as medicine and raw materials for the RMG sector, of necessary hard currency.

The Bangladesh power generation is heavily reliant on furnace oil and diesel-fired IPPs (Independent Power Producers) to meet peak demand.

-

The Subsidy Burden: At $111/barrel, the gap between the cost of generation and the retail price of electricity is vast. If the government passes these costs to the consumer, inflation will skyrocket. If the government absorbs the cost, the fiscal deficit will become unsustainable.

-

The Return of Load Shedding: We are likely to see a return to ‘Industrial Rationing’. To save the grid, the government may be forced to cut power to residential areas and non-essential industries, threatening the productivity of the Ready-Made Garment (RMG) sector, which is the backbone of our export economy.

Diesel is the lifeblood of agriculture in Bangladesh.

-

Irrigation Costs: More than 1.2 million diesel-operated pumps are used for irrigation. A spike in diesel prices directly translates to higher prices for Boro rice and other staples.

-

Transportation Inflation: Bangladesh’s internal logistics are almost entirely road-based. Higher fuel costs will lead to a ‘Food-Inflation Loop’ where the cost of moving produce from Bogra or Jessore to Dhaka becomes more expensive than the produce itself.

While the immediate outlook is bleak, a critical analysis suggests that the UAE’s exit might offer a narrow window for ‘Energy Diplomacy’ for Dhaka. But, that opportunity has to be handled carefully.

Outside of OPEC, the UAE is no longer bound by production caps. ADNOC is hungry for long-term, stable buyers to justify its capacity expansion. Bangladesh, with its growing industrial base, could potentially negotiate a Long-Term G2G Deal with the UAE. By offering Abu Dhabi a guaranteed market share and potential investment opportunities in Halal Product Chail in the Economic Zones (EZs) could secure ‘Preferred Buyer’ status, potentially bypassing the volatility of the spot market.

The UAE’s exit might trigger a ‘Price War’ between Riyadh and Abu Dhabi. While this sounds good for buyers (lower prices), in a war-torn Gulf, a price war often leads to less investment in security and infrastructure, making the supply chain even more fragile. Furthermore, if OPEC collapses entirely, the world loses the only entity capable of ‘flooding the market’ to cool down prices during a global crisis.

The Strategic Roadmap for Bangladesh

Dhaka cannot afford to be a passive victim of the ‘New Oil Order’. The Ministry of Power, Energy, and Mineral Resources (MOPEMR) must adopt a wartime footing, includiing but not limited to.

A. Expanding Strategic Petroleum Reserves (SPR)

Bangladesh currently has a storage capacity of roughly 30–45 days. This is insufficient for the 2026 reality. We must fast-track the construction of the Eastern Refinery Unit-2 and increase storage capacity to push our national reserve to at least 90 days.

B. Beyond the Gulf: Diversification of Origin

The Hormuz disruption proves that ‘all eggs in the Middle Eastern basket’ is not a sustainable strategy. Bangladesh must look toward:

-

Central Asian Pipelines: Exploring links through India to access Turkmen or Kazakh gas.

-

The Americas: Increasing the mix of U.S. West Coast or Brazilian crude, which does not have to pass through the Middle Eastern chokepoints.

C. The Renewable and Nuclear Pivot

The $111 oil price is the strongest possible argument for the ‘Rooppur Nuclear Power Plant’ and its successors. Every megawatt generated by nuclear or solar is a megawatt that doesn't require a dollar-denominated fuel import. The government should immediately waive all duties on industrial-scale solar components and its storage systems.

D. Domestic Gas: The ‘Blue Economy’ Must Become a Reality

For too long, offshore exploration in the Bay of Bengal has been stalled by bureaucratic inertia and unattractive PSC terms. With global energy prices at record highs, the ‘New Oil Order’ makes our offshore blocks more attractive than ever. We must launch a massive, transparent international bidding round with terms that reflect the urgency of our national survival.

E. The Unexplored Phulbari Coal

Amidst the volatility of global energy markets and the debilitating strain on foreign exchange reserves, the strategic development of the Phulbari Coal Mine offers a localized solution to Bangladesh’s energy trilemma of security, equity, and sustainability. Often described as a ‘sleeping giant’, this high-grade bituminous coal reserve could serve as a critical hedge against the $111-per-barrel oil reality, providing a reliable and low-cost baseload for the national grid. By adopting modern, environmentally conscious mining technologies, such as advanced land reclamation and water management systems, Bangladesh could unlock this domestic treasure to fuel its industrial heartlands. Tapping into Phulbari would not only reduce the massive drainage of US dollars spent on fuel imports but also ensure that the nation's economic growth remains powered by its own soil, providing a much-needed buffer against the tremors of a fracturing global oil order.

Navigating the Uncharted

The UAE’s exit from OPEC marks the transition from a world of ‘Energy Order’ to a world of ‘Energy Realism’. In this new era, alliances are transactional, geography is a weapon, and self-reliance is the only true security.

Bangladesh stands at a crossroads. The shocks of 2026, the $111 oil, the Hormuz blockade, and the fracturing of OPEC, are an Acid Test for our nation. If we respond with the same reactive policies of the past, we risk a ‘lost decade’ of economic stagnation. However, if we use this crisis to fundamentally decouple our economy from the whims of global oil cartels, by embracing high quality domestic coal, domestic gas, nuclear energy, and aggressive renewables, we can emerge from this storm as a more resilient, sovereign, and prosperous nation.

The ‘New Oil Order’ is in place and it is the time for Bangladesh to write its own rules.

GSM Shamsuzzoha (Nasim), Online Editor, Energy & Power