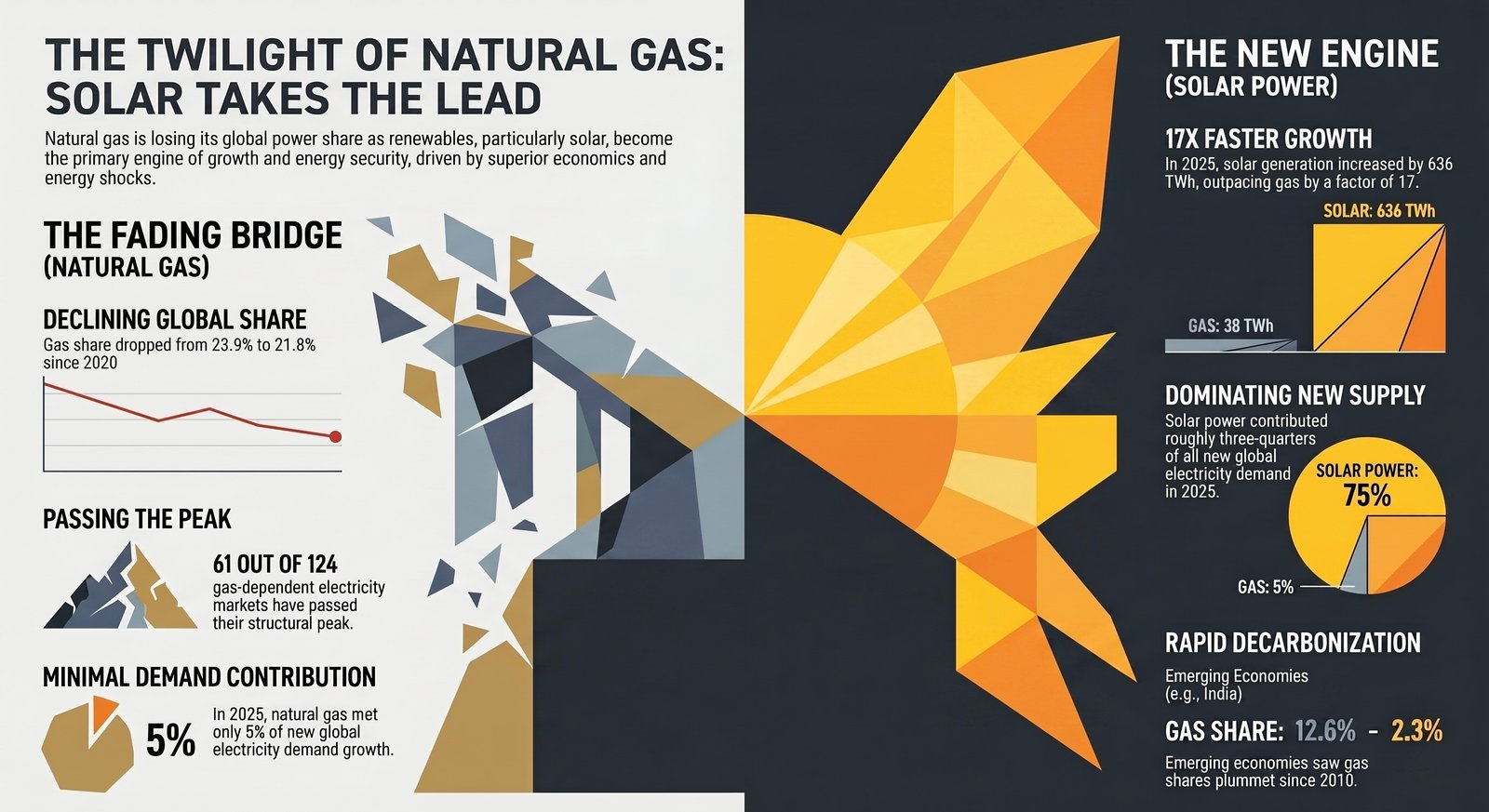

The global power sector is undergoing a clear structural transition as natural gas steadily loses share in electricity generation for the fifth consecutive year. According to analysis from the energy think tank Ember, gas generation has continued to grow slightly in absolute terms, but its share of the global electricity mix has declined from 23.9% in 2020 to 21.8% in 2025.

This shift is being driven primarily by the rapid expansion of solar and wind power, which are increasingly meeting new electricity demand at lower cost and with faster deployment timelines than fossil fuel-based generation. The data indicates that 61 out of 124 gas-dependent electricity markets have already passed their peak gas generation, including major advanced economies such as the UK, Germany, Italy, and Japan.

Key drivers include post-crisis energy security concerns, particularly following geopolitical shocks in 2022 and 2026, improving renewable economics, and the ability of emerging economies to expand electricity access without heavy reliance on gas infrastructure.

Declining Role of Gas in the Global Power Mix

Natural gas is losing momentum in the electricity sector despite continued demand growth.

• Gas share in global electricity has declined every year since 2020

• Growth in gas generation (2021–2025) is roughly half the pace of 2016–2020

• In 2025, gas added only 38 TWh, contributing just 5% of new global electricity demand growth

While gas is still expanding in some regions, its role as the default “bridge fuel” is increasingly weakening.

Solar Power Leads Global Electricity Expansion

Solar energy has emerged as the dominant driver of new electricity supply, significantly outpacing gas.

In 2025:

• Solar generation increased by 636 TWh

• Gas increased by only 38 TWh

• Solar grew about 17 times faster than gas

• Solar contributed roughly three-quarters of new electricity demand growth, while gas contributed only about 5%

This marks a fundamental shift in which renewable energy is no longer supplementary but the main engine of global electricity expansion.

Geopolitical and Economic Forces Reshaping Energy Systems

The decline of gas is being reinforced by structural economic and geopolitical changes.

Energy security shocks, particularly the 2022 Russia–Ukraine conflict and the 2026 Middle East disruptions, exposed vulnerabilities in LNG-dependent systems and triggered renewed investment in domestic renewable energy capacity.

At the same time, declining costs of solar and wind have strengthened their competitiveness. In many regions, domestically produced clean electricity is now seen as more stable, faster to deploy, and less exposed to global price volatility than gas.

Regional Trends and Market Divergence

G7 Economies: Transition Past Peak Gas

Several advanced economies have already passed structural peaks in gas generation. Four G7 members—the UK, Germany, Italy, and Japan—are among the countries that have reached this milestone.

In 2025:

• G7 gas generation fell by 50 TWh

• Renewable generation increased by 123 TWh

• Clean electricity now exceeds fossil-based generation across the G7

United States: A Global Outlier

The United States remains the largest single driver of global gas generation, accounting for around 26% of global output in 2025, and has contributed significantly to global gas growth over the past decade.

Emerging Economies: Low Gas Dependence

Despite rapid demand growth, several large emerging economies have limited reliance on gas:

• India: Gas share declined from 12.6% (2010) to 2.3% (2025)

• Brazil: Fell from 13.7% peak (2014) to 7.3%

• China: Maintains ~3% gas share despite massive demand expansion

These trends reflect a broader pattern of electrification driven increasingly by renewables rather than fossil gas.

Conclusion

Global electricity systems are approaching a decisive inflection point in gas generation. While gas remains part of the energy mix, its strategic role is diminishing as countries prioritize affordability, energy security, and domestic generation capacity.

The evidence points to a long-term trajectory where clean electricity—particularly solar and wind—becomes the primary driver of global power system growth, gradually marginalizing gas in both developed and emerging markets.