The newly elected Government of Bangladesh has formulated a comprehensive Five-Year Work Plan (2026–2030) aimed at restoring momentum in the energy and mineral resources sector, strengthening national energy security, and supporting sustained economic growth. The strategic roadmap places strong emphasis on accelerating domestic gas exploration, expanding LNG and fuel infrastructure, and advancing critical institutional and policy reforms. By prioritizing the timely finalization of production sharing contracts (PSCs), increasing drilling capacity, and modernizing refining, transmission, and distribution systems, the plan seeks to ensure a reliable and affordable energy supply while improving overall operational efficiency across the sector.

At the core of the plan is a phased and carefully sequenced approach to augmenting gas production. This includes a target to drill as many as 180 wells by 2028, alongside the launch of deep exploration initiatives to unlock untapped hydrocarbon potential. In parallel with upstream development, the government is prioritizing expansion of the national gas transmission network and the installation of major LNG infrastructure, including both floating storage and regasification units (FSRUs) and land-based terminals. The plan also incorporates modernization of the distribution segment through the large-scale rollout of smart prepaid gas meters and the integration of advanced SCADA systems to enable real-time monitoring and improved system management.

Beyond infrastructure expansion, the 2026–2030 period is expected to bring significant institutional restructuring. A key reform measure includes the division of Titas Gas Transmission and Distribution PLC into three separate entities to enhance governance, accountability, and operational efficiency. Similarly, the Bangladesh Petroleum Corporation (BPC) is set to undergo restructuring to streamline its organizational framework. In addition, the government has outlined a phased Coal Development Plan for the Barapukuria coalfield and has committed to investing in research and development of alternative energy sources, including green hydrogen and geothermal energy. Taken together, these initiatives are designed to position Bangladesh to meet rising energy demand while gradually transitioning toward a more diversified and resilient energy mix.

Through these wide-ranging initiatives, the government aims to ensure a stable and affordable energy supply, enhance efficiency across the sector, and support the country’s rapidly expanding economic activities, while laying the groundwork for a more secure and sustainable energy future.

Enhancement of Gas Production

To strengthen domestic gas supply, the government has undertaken an ambitious and multi-year drilling program. In 2023, drilling operations were planned for 50 wells, of which 25 wells have already been completed. These completed wells have added approximately 252 MMCF of gas per day to the system, with around 129 MMCF per day already connected to the national gas grid and contributing to supply.

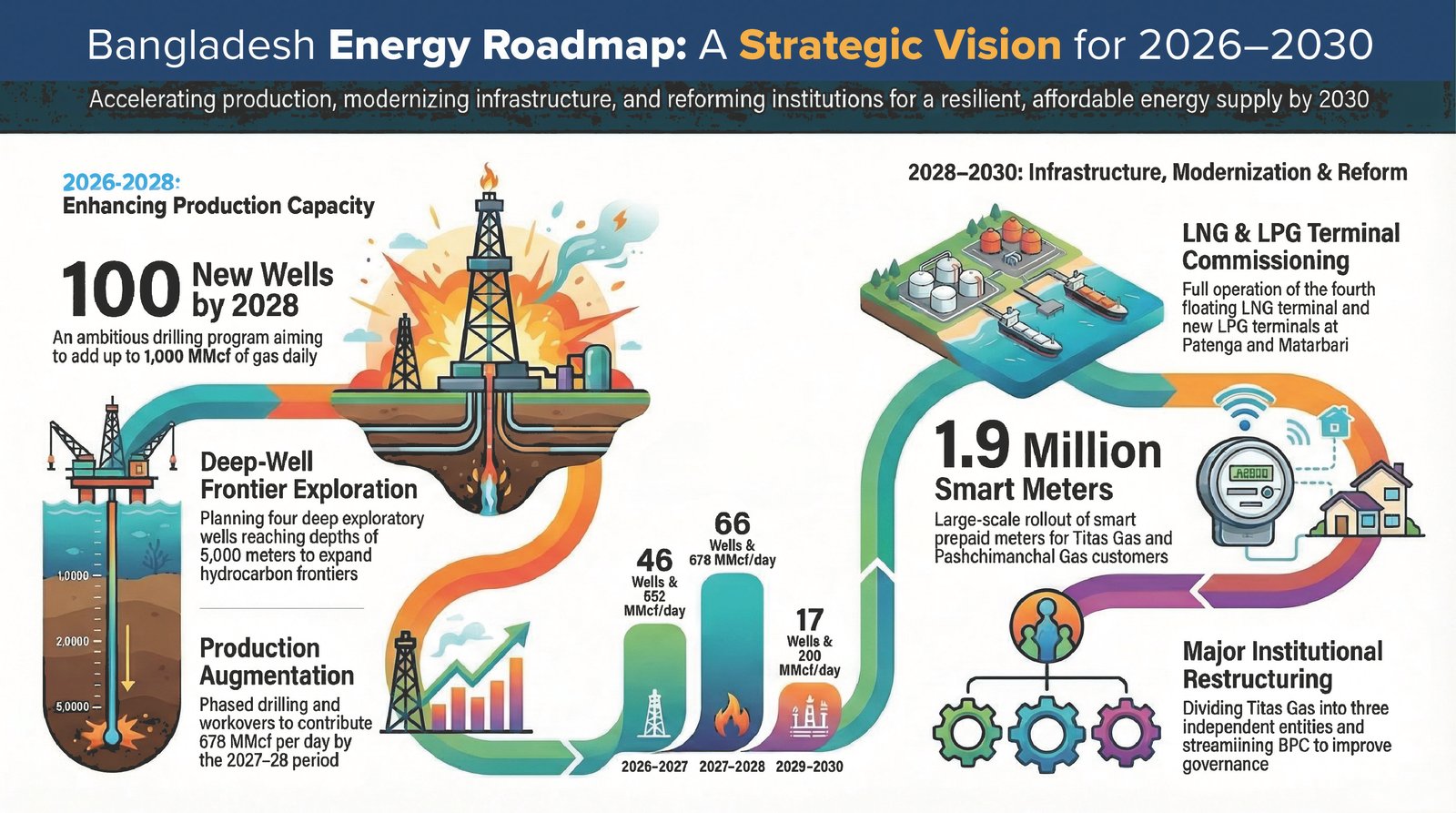

Looking ahead, the government has set an even more ambitious target of drilling 100 wells by 2028. If successfully implemented, this program could potentially add up to 1,000 MMCF per day to the national gas supply system, significantly easing supply constraints. To support this expansion in exploration and production activities, plans are underway to procure two new drilling rigs for BAPEX, thereby strengthening its operational capacity. In addition, four deep exploration wells, each reaching depths of approximately 5,000 meters, are planned. These deep wells are expected to play a critical role in expanding Bangladesh’s hydrocarbon exploration frontier and identifying new reserves.

Gas Production Augmentation Program

A structured and phased gas production augmentation plan has been developed to increase national supply over the period from 2026 to 2030. Under the initial 180-day program, an additional 50 MMCF per day of gas will be added to the national grid. During this phase, detailed project proposals covering seven exploration wells, seven development wells, and two workovers will be prepared and submitted to the Planning Commission for approval.

During the 2026–2027 period, drilling activities will cover a total of 46 wells, including eight workovers, with the objective of adding approximately 652 MMCF per day to the grid. In the subsequent period of 2027–2028, drilling operations will expand further, with 66 wells—including 23 workovers—expected to contribute an additional 678 MMCF per day. Finally, between 2028 and 2030, drilling of 17 wells is projected to add around 200 MMCF per day to the national gas supply system. This phased approach reflects a steady and incremental strategy to close the supply-demand gap.

Oil and Gas Exploration under Production Sharing Contracts

The plan for oil and gas exploration under PSCs spans the period from 2026 to 2030. As part of the initial 100-day program, the government will finalize a model PSC applicable to both onshore and offshore exploration. This is expected to provide greater clarity and attract investment from international oil companies (IOCs).

In fiscal year 2026–27, bidding rounds will be invited for both onshore and offshore oil and gas exploration blocks. During 2027–28, contracts will be signed with selected IOCs. From 2028 to 2030, the government will maintain active monitoring to ensure that exploration activities progress according to schedule and that production commences within the timeframes stipulated in the PSC agreements. This structured timeline is intended to ensure accountability and timely development of resources.

LNG Infrastructure Development

To enhance energy supply stability, the government has launched a comprehensive LNG infrastructure development program. Under this plan, a fourth floating LNG terminal (FSRU) is proposed at Kutubjom in Maheshkhali. The project will undergo review during the initial phase, with agreements expected to be finalized during 2026–2027. Installation is planned for 2027–2028, with full commercial operation anticipated between 2028 and 2030.

In parallel, a land-based LNG terminal will be developed under a Public-Private Partnership (PPP) framework. Preparatory activities, including the appointment of a transaction adviser, preparation of tender documents, and updated feasibility studies, are expected to be completed by 2026–2027. Construction and commissioning of the terminal are projected for the 2028–2030 period. Additionally, proposals will be invited for another floating LNG terminal in the deep-sea region of southern Bangladesh, further strengthening the country’s LNG import capacity.

Expansion of Gas Transmission Pipeline Network

The government has also initiated a major expansion of the gas transmission pipeline network to support both domestic production and imported LNG. During the initial 180-day period, an integrated plan will be adopted to connect gas resources from Bhola to the national grid while preparing infrastructure for future LNG imports.

Feasibility studies will be conducted for key pipeline routes, including Barisal–Aminbazar, Barisal–Khulna, and Barisal–Bhola. Between 2026 and 2027, the implementation framework for the Bhola–Barisal–Aminbazar pipeline will be finalized, and construction activities will begin. Installation will continue through 2027–2028, with the pipelines expected to be completed and commissioned during 2028–2030. This expansion is critical for improving supply distribution and regional connectivity.

Development of LPG Terminals at Patenga and Matarbari

The government has prioritized the development of LPG terminals at Kattoli in Patenga and at Matarbari in Cox’s Bazar as part of its broader energy security strategy. These projects are intended to ensure a reliable LPG supply, diversify the national fuel mix, and reduce dependence on depleting natural gas reserves.

For the Patenga LPG terminal, a pre-feasibility study will be conducted and a memorandum of understanding (MoU) signed within the first 180 days. During this period, the implementation modality – whether government-to-government (G2G), PPP, or other models – will be determined. By 2026–27, land transfer will be facilitated, feasibility studies completed, and consultants appointed, followed by international tendering. In 2027–28, an EPC contract will be signed and the Front-End Engineering Design (FEED) approved. Construction of storage tanks, jetties, and pipelines will take place during 2028–2030, followed by commissioning.

A similar approach will be followed for the Matarbari LPG terminal. Initial studies and agreements will be completed within the first 180 days, followed by land development, dredging, tendering, and construction. The terminal is expected to be operational by 2030, significantly strengthening the country’s LPG infrastructure.

Government Management of LPG Import

Under the initial 180-day plan, proposals from various institutions regarding LPG import and management will be reviewed, and implementation modalities will be determined. During FY2026–27, agreements will be signed and land acquisition for infrastructure development will be completed.

From FY2027 to FY2030, a structured system for LPG import and market management will be introduced, ensuring efficient supply, distribution, and regulatory oversight. This initiative aims to strengthen energy security while improving market discipline.

Smart Meter Installation and Digitalization

The government plans to modernize the gas distribution system through large-scale smart metering and digital monitoring. Under this initiative, smart prepaid gas meters will be installed for 1.75 million customers under Titas Gas, 128,000 customers under Pashchimanchal Gas Company Limited, and 50,000 customers under Jalalabad Gas.

In addition, SCADA systems across Petrobangla and its subsidiaries will be integrated to enable real-time monitoring, improve operational efficiency, and enhance overall system management.

Institutional Reforms in the Energy Sector

Institutional restructuring forms a key component of the reform agenda. The government plans to divide Titas Gas into three separate companies by 2030 to improve governance and efficiency. Similarly, BPC will be restructured to reduce the number of subsidiary companies from eight to five by 2026, streamlining operations and strengthening oversight.

Barapukuria Coal Mine Expansion Plan

The Barapukuria Coal Mine Expansion Plan has been structured as a phased roadmap. Within the first 180 days, techno-economic feasibility studies for open-pit mining will be initiated. These studies will continue through 2026–27, providing essential data for decision-making.

In 2027–28, feasibility studies will be completed, development projects formulated, and initial extraction activities launched. Based on these results, commercial production is expected to begin during 2028–2030, marking a transition to full-scale operations.

Alternative Energy

During the initial phase, feasibility studies will assess the viability of alternative energy sources. In 2026–27, research will focus on advanced technologies, including coal bed methane, underground coal gasification, coal-to-liquid conversion, and green hydrogen.

The outcomes of these studies will guide implementation, while private sector participation will be encouraged through investment opportunities.

Observations

The Five-Year Work Plan (2026–2030) sets out an ambitious and well-structured vision for Bangladesh’s energy sector. On paper, it addresses many of the country’s long-standing weaknesses – limited domestic exploration, infrastructure gaps, and institutional inefficiencies. But as with many plans before it, the real challenge will lie in execution. Delivering on such a wide-ranging agenda within tight timelines will require not only strong political commitment but also coordination across multiple agencies that have historically struggled to work in sync.

One of the most pressing concerns remains the growing mismatch between energy demand and domestic supply. Bangladesh’s economy continues to expand, and with it, energy consumption. Yet domestic gas production has not kept pace. This gap has increasingly been filled by imported LNG, exposing the country to global price volatility and supply uncertainties. The current LNG import capacity, around 1,100 MMCFD, falls well short of what is needed. Without a significant and timely expansion, supply shortages are likely to persist, especially during peak demand periods.

The delays and cancellations of LNG infrastructure projects in recent years have compounded the problem. Large-scale projects such as land-based LNG terminals require long gestation periods, often five to seven years. Any hesitation or policy inconsistency today will translate into supply constraints several years down the line. This makes early decision-making and continuity in implementation particularly important.

In the upstream segment, attracting international oil companies has become more difficult. The global energy landscape is evolving, with companies becoming more selective about where they invest. Bangladesh, offering a limited number of offshore blocks under conventional bidding frameworks, may not appear sufficiently competitive. At the same time, domestic exploration efforts have yet to fully reflect the country’s geological potential. Areas such as Chhatak remain underexplored despite indications of significant reserves.

Coal remains another unresolved issue. Bangladesh possesses sizable coal deposits, yet policy indecision has kept these resources largely untapped. The Phulbari coal project, for instance, has been under discussion for years without a clear outcome. This lack of direction creates uncertainty and limits the country’s ability to diversify its energy mix and reduce reliance on imports.

Overall, while the plan is comprehensive, it highlights a familiar pattern: strong intent but persistent structural and policy constraints. Unless these underlying issues are addressed, even the most well-designed roadmap may struggle to deliver its intended results.

Way Forward

Moving forward, the government’s immediate priority should be to translate plans into action, particularly in the area of domestic gas exploration. Strengthening national institutions such as BAPEX and Petrobangla is essential – not just in terms of equipment, but also in building technical expertise and decision-making capacity. Faster drilling, better data, and more efficient project execution will be key to narrowing the supply gap.

At the same time, expanding LNG import capacity cannot be delayed. Given the long lead times involved, decisions taken today will determine supply conditions several years from now. Revisiting previously canceled or stalled LNG agreements could offer a quicker path forward, as renegotiating existing frameworks is often faster than starting from scratch. Ensuring that transmission and distribution networks are ready to handle increased imports will also be critical.

In offshore exploration, a more flexible approach may be necessary. Rather than relying solely on traditional bidding rounds, the government could consider direct negotiations with major international energy companies and offer a larger portfolio of blocks. This would make Bangladesh a more attractive destination for investment in a highly competitive global market.

There is also a need to move quickly on high-potential exploration areas. Conducting detailed seismic surveys in regions like Chhatak and following up with timely drilling could yield faster results than waiting for large-scale offshore developments. Small but early successes in such areas can help build momentum and confidence.

Perhaps most importantly, the government must take a clear and consistent position on coal. Whether the decision is to develop these resources or to move away from them, clarity is essential. If development is pursued, projects like Phulbari should be reviewed independently and implemented with modern, environmentally responsible technologies. If not, the country must plan accordingly for alternative sources to fill the gap.

In the broader context, Bangladesh will need a balanced energy strategy – one that combines domestic resource development, reliable imports, institutional reform, and gradual adoption of cleaner energy sources. Just as important as the strategy itself is the ability to maintain policy continuity and follow through on commitments. In the end, steady and disciplined implementation, rather than ambitious planning alone, will determine whether the country can achieve a more secure and sustainable energy future.

Mortuza Ahmad Faruque, Energy Expert and Former Managing Director of BAPEX

Download Special Article As PDF/userfiles/EP_23_20_SA.pdf