The suspension of the Switzerland-hosted implementation talks between Iran and the United States has injected fresh uncertainty into global energy markets, slowing the recent decline in oil and liquefied natural gas (LNG) prices and raising concerns over shipping costs through the strategically vital Strait of Hormuz. Although energy markets had initially welcomed the Iran-US agreement that ended weeks of conflict, the postponement of follow-up negotiations and renewed fighting in Lebanon have reminded traders that geopolitical risks in the Middle East remain far from over. Source Agencies and Online.

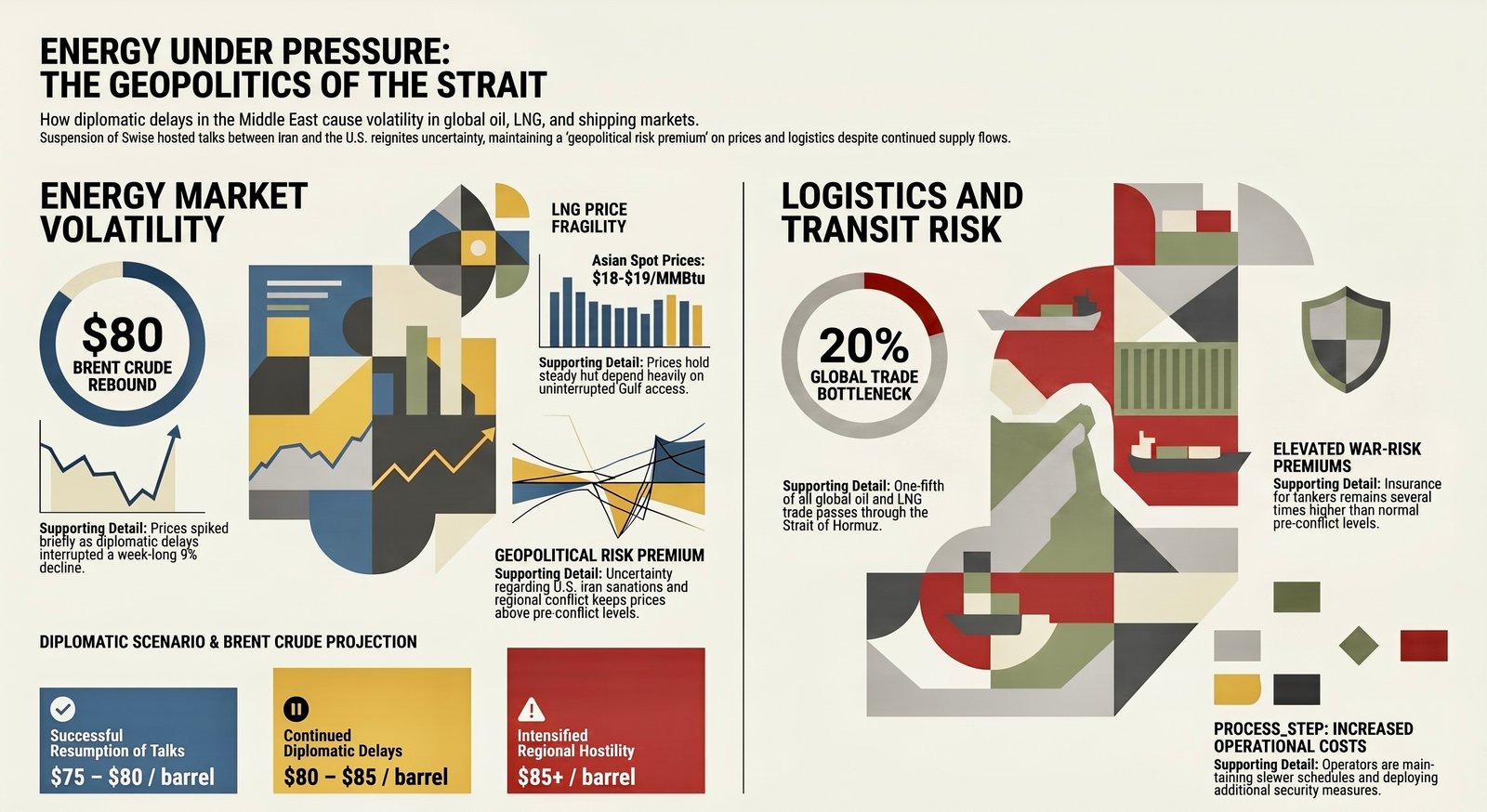

Global crude oil prices, which had fallen sharply after the announcement of the ceasefire and the reopening of parts of the Strait of Hormuz, have become volatile once again. Brent crude, which had dropped below $79 per barrel, briefly rebounded to around $80 per barrel after news emerged that US Vice President JD Vance had postponed his trip to Switzerland, raising doubts about the pace and durability of the diplomatic process.

Despite the short-term recovery in prices, oil remains significantly below the highs recorded during the peak of the Iran-Israel conflict. Brent crude is still on course for a weekly decline of nearly 9 percent as oil shipments gradually resume through the Strait of Hormuz. However, analysts caution that any prolonged delay in diplomatic engagement could quickly restore a geopolitical risk premium to the market. Approximately 20 percent of global oil and LNG trade passes through the Strait of Hormuz, making any disruption there an immediate concern for international energy security.

AI-Assisted Infrographic

The LNG market has also entered a more cautious phase. Asian spot LNG prices, measured by the Japan-Korea Marker (JKM), have stabilized around $18-$19 per million British thermal units (MMBtu) in recent weeks after retreating from earlier conflict-driven highs. However, traders are closely monitoring the diplomatic situation because LNG cargoes originating from Qatar and the Gulf region remain heavily dependent on uninterrupted access to Hormuz.

Market participants say buyers in Asia, particularly Japan, South Korea, China, India and Bangladesh, may become more active in securing additional cargoes if negotiations remain stalled for an extended period. Such precautionary buying could put upward pressure on spot LNG prices during the coming weeks, especially ahead of peak summer electricity demand in Asia.

Shipping costs are also beginning to rise again. Although maritime restrictions have eased since the ceasefire, insurers and shipping companies continue to classify the Gulf region as a high-risk area. War-risk insurance premiums remain elevated, and tanker operators are still charging additional fees for voyages passing through Hormuz.

Industry analysts estimate that insurance costs for Very Large Crude Carriers (VLCCs) and LNG vessels remain several times higher than normal pre-conflict levels. Some shipping companies are maintaining slower sailing schedules and deploying additional security measures, increasing overall transportation expenses for both crude oil and LNG deliveries.

The impact is particularly important for LNG-importing countries in South Asia. Bangladesh, Pakistan and India could face higher procurement costs if shipping disruptions persist, especially because a large portion of their imported LNG originates from Qatar.

Energy economists argue that the suspension of the Swiss talks has not yet triggered a supply crisis, but it has interrupted the process of rebuilding market confidence. The greatest risk now is uncertainty rather than an immediate shortage of energy supplies.

Another key issue is the future implementation of the Iran-US agreement itself. The deal envisaged the eventual removal of US sanctions on Iranian oil exports and the gradual return of additional Iranian crude supplies to global markets. Analysts estimate that the release of millions of barrels of previously constrained oil could eventually create a more balanced market and put downward pressure on prices. However, delays in negotiations could postpone those benefits.

Looking ahead, energy markets are expected to remain highly sensitive to political developments. If Switzerland-hosted talks resume quickly and tensions in Lebanon ease, Brent crude could stabilize within a $75-$80 per barrel range and LNG prices may remain relatively contained. Conversely, if diplomatic delays continue and regional hostilities intensify, oil could move back above $85 per barrel, LNG prices could rise again, and shipping costs would likely remain elevated throughout the summer period.

For now, the suspension of the Swiss talks has not reversed the broader trend of improving energy flows, but it has served as a reminder that the Middle East remains the world’s most critical geopolitical risk zone for global energy security. Until diplomacy regains momentum, oil traders, LNG buyers and shipping companies are likely to continue pricing in a significant level of uncertainty.