The global natural gas market outlook has been significantly reshaped by the ongoing Middle East conflict, with major disruptions to supply chains delaying an anticipated wave of liquefied natural gas (LNG) expansion, according to the latest quarterly report by the International Energy Agency (IEA).

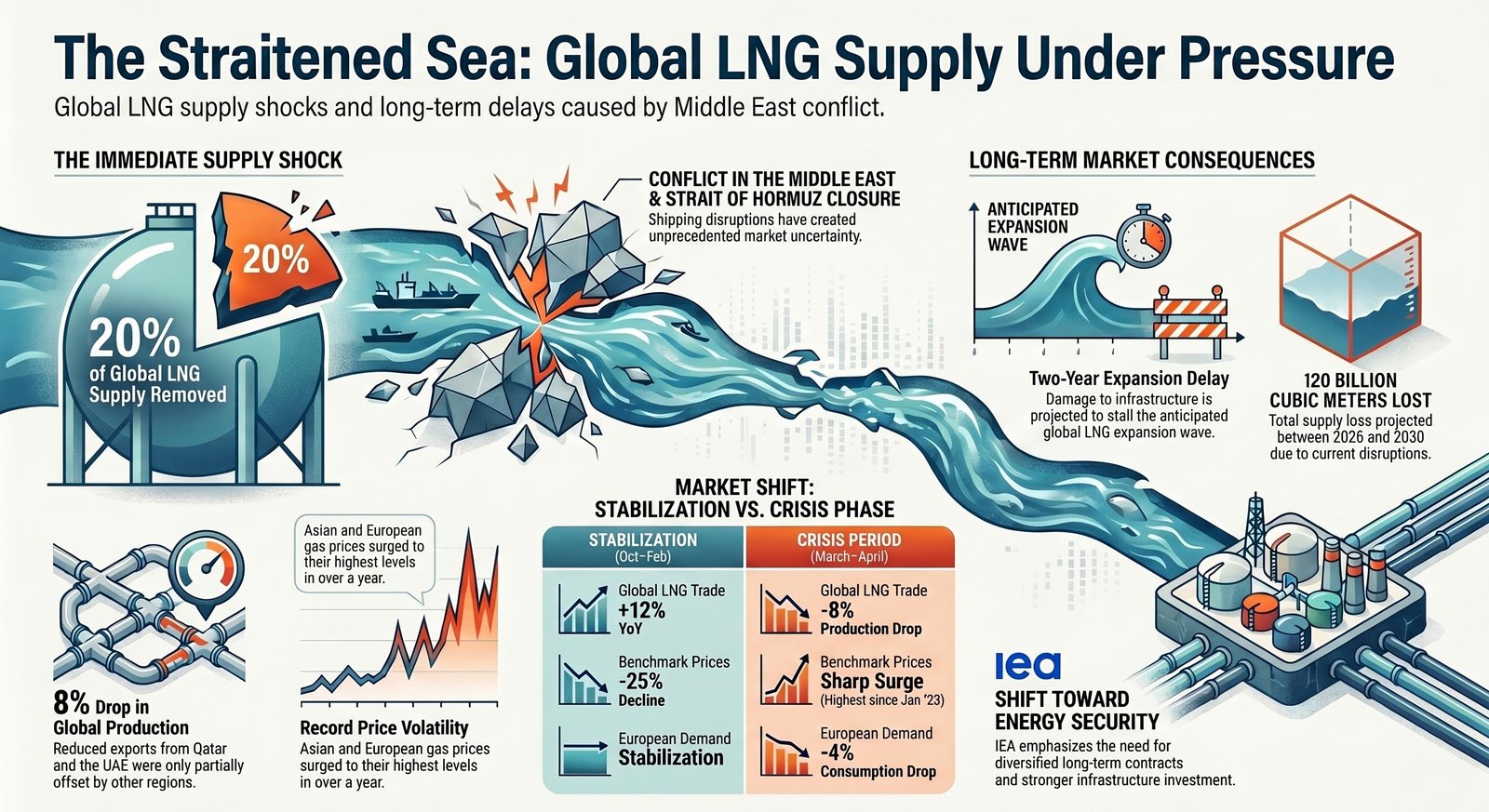

The report highlights that shipping disruptions through the Strait of Hormuz since early March have created unprecedented uncertainty, temporarily removing nearly 20% of global LNG supply from the market. This has triggered sharp price increases across key importing regions.

During a period of intense volatility in March, natural gas prices in Asia and Europe surged to their highest levels since January 2023, leading to reduced demand in major LNG-importing markets.

The crisis has reversed a recent trend of market stabilization observed during the 2025–26 winter season, when strong growth in LNG supply—particularly from North America—helped ease prices. Global LNG trade rose by 12% year-on-year between October and February, while benchmark prices in Europe and Asia declined by around 25% during that period.

However, extreme weather events, including winter storms across North America, Europe, and East Asia, drove spikes in demand, underscoring the importance of flexible gas supply systems—especially as renewable energy’s share continues to grow.

Market conditions shifted sharply in March as the Middle East conflict effectively halted LNG shipments through the Strait of Hormuz. As a result, global LNG production dropped by 8% year-on-year, with reduced exports from Qatar and the United Arab Emirates only partially offset by increased output elsewhere. Supply disruptions deepened in April, with further declines in LNG deliveries.

Higher prices, milder weather, and conservation policies have since reduced gas demand in key markets. In Europe, consumption fell by about 4% year-on-year in March, supported by increased renewable energy generation. Several Asian countries have also introduced fuel-switching strategies and demand-side measures to curb gas use.

Beyond immediate disruptions, the crisis is expected to have longer-term implications. Damage to LNG infrastructure in Qatar is projected to slow supply growth and delay the global LNG expansion wave by at least two years. Overall, the market could lose around 120 billion cubic meters of LNG supply between 2026 and 2030.

While new projects in other regions may eventually offset these losses, the supply gap is likely to keep global gas markets tight through 2026 and 2027.

The IEA emphasized the need for stronger investment across the LNG value chain and greater international cooperation to enhance energy security. It also noted that diversified long-term supply contracts can help countries better manage price volatility during periods of disruption.