The demand for power and energy has dropped substantially due to COVID-19 pandemic, but it offered a rare and unique opportunity for the sector to reassess the priorities. The present coincident peak demand for power is not more than 8,000 MW while gas demand would not be over 2,000 MMCFD. The grid-connected power generation capacity without captive generation is now about 20,000 MW. The capacity of natural gas supply with imported 1,000 MMCFD RNLG is 3,700 MMCFD. With most of the major industries remaining shutdown and commercial enterprises remaining partially locked down, the situation offers unique opportunities for power and energy sector planning and carrying out much needed overhauling and maintenance. At this stage, it is unsure when business as usual will resume and when the demand would increase again. But it is almost certain that with Europe and North America being severely affected, most of the export-oriented industries in Bangladesh may not be able to resume full-capacity production at least in the next 2-3 months. The coronavirus has also affected implementation of the mega energy, power and infrastructure development projects of the country. Some large power projects, land-based LNG terminal construction and projects in power transmission and distribution would be delayed at least by a year or so depending on how long the crisis would continue.

The Energy & Power Magazine in its last issue published on April 1, 2020 has extensively discussed on how the COVID-19 has already affected the power and energy projects. This write up would rather discuss on the smart responses by the sector in the present and emerging circumstances.

Present Demand-Supply Scenario

The MOPEMR has so far successfully managed seamless supply of power and energy to all users during these difficult days. Of course, the reduced demand resulted in surplus generation of power and more than required production and supply capacity of natural gas facilitated this. But one must appreciate the commitment of energy and power sector officials who are ensuring the security of supply along all segments of power and energy value chain so far. The Prime Minister could carry out video conference with 64 districts simultaneously without any interference due to power glitch is a testimony to this. There has been no incident of loadshedding or gas system low pressure. Credit must be given to the unsung heroes of power and gas system operators.

Power Demand-Supply Scenario

The installed capacity of grid-connected power, including 1,160 MW import from India, now is 19,570 MW. Taking into consideration the 2,800 MW of captive power and 357 MW off-grid solar power, the total capacity is 22,727 MW. On March 25, the power system was ready for managing 12,679 MW on average and 15,173 MW at peak. But on March 24, the actual demand was over 8,812 MW on average and 10,264 MW at peak. Of course, most of the industries which were in operation obviously were using captive power.

The present situation has created a very rare opportunity for public sector power plants to carry out much required maintenance of the ageing power plants. PGCB can also check the actual impacts of shutting down several liquid fuel-based contingency power plants in a programmed manner. Power distribution utilities could expedite working in installation of the prepaid meters. This is a time to test with most fuel-efficient power plants. It can be expected that the Power Division can now workout much better on how to phase out contingency power plants. Policymakers must not be encouraged from falling petroleum products price in the global market as the crude price would soar again as soon as the COVID-19 effects start easing. The delays in the construction of major power plants may not affect much as the demand is not growing. System planners must continue discussions with the industries on how they can start using grid power instead of captive generation. If necessary, a preferential tariff can be offered. Industries would need fiscal and financial incentives in any case.

The power sector planners must also review fuel options. It has already been observed that importing coal and transporting them to Payra and Rampal would not be so easy. Additional cost of transportation would have a major impact on the generation cost. The government should seriously review giving green signal to mining own coal and using railway system with considerable upgrade to carry own coal for power plants at Payra and Rampal. PGCB also gets breathing space to complete its power transmission grid expansion projects and other outstanding works.

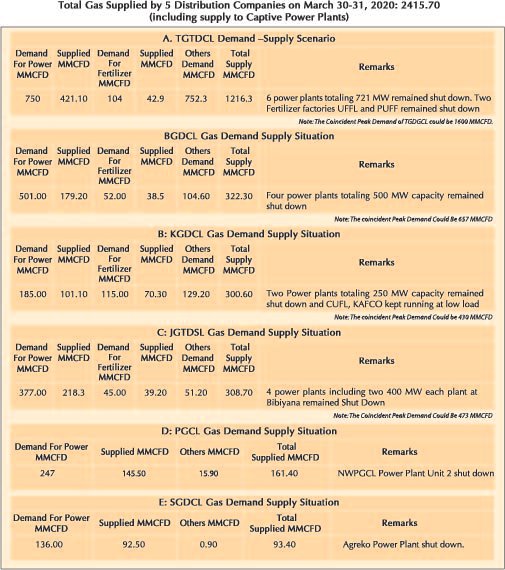

Gas Demand-Supply Situation

The reduced demand for power and reduced demand in industries have also given a breathing space for the gas system as well. GTCL has already completed the remaining works of Moheshkhali–Anowara 42 inches OD gas transmission loop line and Faujdarhat–Feni–Bakhrabad 36 inches OD gas transmission pipeline construction. Gas grid is now ready for evacuating 1,000 MMCFD RLNG from two private sector-operated FSRUs.

The gas production and supply report of Petrobangla (Bangladesh Oil gas and Mineral Corporation) on March 30-31 states that the gas system has a production and supply capacity of 3,760 MMCFD. It included 1,145 MMCFD from 70 wells of 17 gas fields owned and operated by three Petrobangla companies BGFCL, SGFL and BAPEX. Two IOCs Chevron and Tullow from 43 wells in four gas fields can supply 1,615 MMCFD. Two FSRUs operated by two privately owned companies can deliver 1,000 MMCFD. On the days, Petrobangla-owned fields supplied 695.80 MMCFD, IOCs supplied 1,080.20 MMCFD and RPGCL led FSRUs supply 602.80 MMCFD RLNG. GTCL transported 2,378.90 MMCFD in its gas grid.

If we review the gas use by distribution companies, we find the following:

It appears that the situation has come as blessing for Petrobangla-owned gas production companies. Petrobangla has to continue purchasing LNG from suppliers and letting FSRUs operate as per the contract. It has also to purchase gas from IOCs under GPSA commitments. In the meantime, it must concentrate on much delayed wellhead compressor installation project of BGFCL. The wellhead pressure of several Titas Gas Field wells is fast depleting. Titas could produce only 268 MMCFD from its 26 wells capable of producing 542 MMCFD. Unless wellhead compressors are set up soon, it would not be possible to continue production of many of these wells. In due course, almost all the producing gas wells of BGFCL would require wellhead compressors. These days, skid-mounted modular wellhead gas compressors are available. Setting up of wellhead compressor must be priority one for Petrobangla-owned gas production companies.

GTCL Must Strengthen Operation Capabilities

The reduced gas demand has also created opportunity for GTCL for giving a fresh look into its major system operation and maintenance. Too many large gas transmission pipeline projects – some necessary and few unnecessary – caused it to divert most of its time and energy on projects implementation. It must put stress on system operation. It is a pity that the SCADA system cannot be completely refurbished yet. The supervisory control cannot be done yet. GTCL franchise now spreads from Moheskhali in the South East to Bogura in the North West, Bibiyana in the North to Khulna in the South. Unless SCADA is fully operational, GTCL cannot manage the system efficiently. GTCL also should have been in a position to operate the compressor stations by now instead of extending the EPCM contract with the contractor. Several officials have attended operation training on compressor station operation in different countries including UK. What are these people doing?

GTCL has done a wonderful job in implementing major projects under challenging circumstances. Now it must prove its excellence in system operation because very soon when circumstances gets back to business as usual, the major challenge would be ensuring security of supply of the gas grid. All new gas supply would come from Chattogram region whether it is RLNG or gas from offshore. As such, there must be strong unit of operation in Chattogram-Cox’s Bazar region.

The present demand-supply situation evidences that no gas from gas grid needs to be supplied for KGDCL franchise area from the central region. Rather RLNG is enough to meet the present requirement and even supply about 500 MMCFD to rest of the grid at least for the next 4-5 years. GTCL must make transmission planning accordingly. It must also plan what to do with its gas compressor station lying almost idle at Elenga. It must also plan how to utilize gas transmission pipeline all the way to Khulna. The government must plan to start supplying gas to industries in Kushtia, Jashore and Khulna region as soon as 1,000 MMCFD RLNG supply starts. We must not leave the Khulna region gas dry indefinitely. The facilities are built in. A company named SGDCL is there. They must be made operational.

Petorbangla Must Plan for Coal Extraction and Expediting Gas Exploration

We are not sure how else the policymakers would understand the necessity of fully exploiting own fuel potential before going exclusive for imported fuel. Natural circumstances like COVID-19 or regional conflicts can disrupt supply chain, make global fuel market volatile. Bangabandhu as anticipated this planned for exploring and exploiting own fuel resources. No smart nation can afford going to imported fuel for volatile uncertain global market leaving its substantially discovered coal reserve and potential petroleum resources unexploited. Unfortunately, the ill-advice has made the policymakers misguided into exclusive coal import strategy which would backfire soon. At this stage going for offshore bidding would not be also appropriate as the IOCs would not risk billions of dollars investment in Bangladesh offshore due to very low crude price. It will be appropriate going for multi-client survey works and waiting till the end of 2020 for offshore bidding. The approval process would take about a year. By that time some useful data may be available. Bangladesh may not achieve SDG7 – sustainable energy supply to all at affordable cost – unless it exploits its own fuel resources to full extent.

What the Gas Distribution Companies Should Do?

This is the time for the gas distribution companies to intensify drive against illegal use of gas. The program for prepaid meter for domestic consumers must also be expedited. With industries mostly not using gas, it must not be difficult tracking in which areas gas thefts are rampant. Many ageold gas distribution networks need phasing out as these have become dilapidated as well. The government should not only give new gas connection in old areas to domestic consumers, it should also phase out domestic supply and replace with LPG.

It is expected that the power and energy sector would utilize this breathing time now to better plan and prepare their future actions. This breathing period must be spent smartly looking at its resources, assessing own technical, managerial and operational capabilities, spending more time in system operation and maintenance. Bangladesh cannot compete with China, Japan. Korea, India and other countries in importing primary fuel from the global market when their will be a surge of demand again in not very distant future to cure the bleeding economic development.

Saleque Sufi;

Contributing Editor, EP