Achieving sustainable energy security and ensuring a subsidy-free, self-sustaining energy and power sector remains a major challenge for Bangladesh. Over the past few years, the government has provided substantial subsidies to both the power and energy sectors. As a condition of the IMF loan, the government is under pressure to completely withdraw subsidies from these sectors.

Given the current condition of the energy and power sector, and based on foreseeable developments, it is unlikely that Bangladesh will achieve a subsidy-free energy sector before 2030. Excessive reserve margins far above actual demand, significant idle capacity obligations, capacity payments, the devaluation of the taka against the US dollar, and increasing reliance on expensive imported fuels are among the main reasons for the sector’s continued dependence on subsidies.

The former government increased power tariffs and fuel prices several times in an attempt to reduce subsidies. However, those efforts have proven inadequate. Considering the ongoing energy crisis, which is severely affecting industrial operations, and the negative impact of unreliable energy supply on investment, the government must take bold, though potentially unpopular, steps to phase out subsidies gradually.

Improving energy efficiency and conservation must be a top priority. Eliminating theft and pilferage from the system, reflected in unacceptable system losses, should also be high on the government’s agenda. Additionally, contracts with Independent Power Producers (IPPs), particularly regarding tariffs, must be reviewed and renegotiated.

The government must also ensure that industrial power demand grows steadily. This requires addressing constraints in power transmission and distribution networks serving industrial zones. Additional demand can be stimulated by promoting the adoption of electric vehicles, increasing the share of renewable energy, and expediting the exploration and development of domestic fuel resources. However, these measures will take at least 3–5 years to yield results. Until then, it is unrealistic to expect a subsidy-free energy sector in Bangladesh.

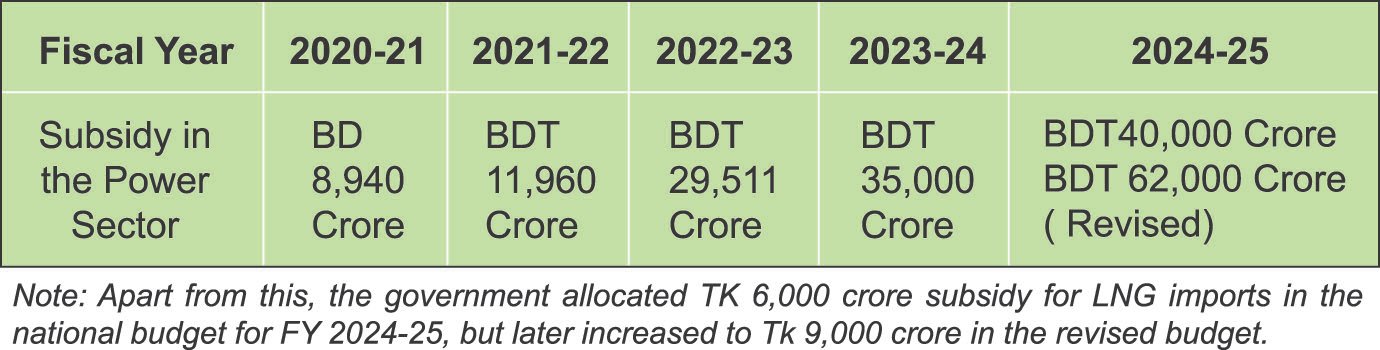

Subsidies in the Power and Energy Sector

According to observers and analysts, energy sector planning and management in Bangladesh have lacked integration. The implementation strategies have often been flawed. A bureaucracy-dominated and corruption-prone system has created a large reserve margin, while chronic shortages in primary fuel supply have resulted in nearly 50% of generation capacity remaining unutilized.

Power generation costs remain significantly higher than the tariff charged to end users. Utilities are burdened by enormous capacity charges. Due to years of neglect, Bangladesh’s energy sector suffers from an unreliable supply of primary fuels. Successive governments have failed to make key political decisions, such as utilizing the country’s coal resources. From 2000 to 2025, only limited onshore and offshore gas exploration was conducted, leading to an alarming depletion of proven gas reserves. As a result, Bangladesh has become increasingly dependent on imported fuels—coal, LNG, and liquid fuels.

All these factors have kept generation costs far above the tariff levels. The BPDB has paid Tk 1.4 trillion in capacity charges alone over the past 15 years. The government is forced to allocate significant subsidies each year to keep state-owned enterprises operational.

Given the current situation and near-term outlook, phasing out subsidies will be a major challenge. The government must develop an actionable, phased plan to reduce dependency on subsidies. This plan must include a comprehensive energy and power system master plan incorporating an affordable fuel mix, a clear fuel utilization policy, energy efficiency and conservation strategies, and large-scale skill development.

In the recent past, the Power Division requested Tk 30,575 crore for development and operations, but the ministry proposed an allocation of only Tk 13,658 crore, excluding subsidies. This can only be managed if the power sector minimizes the cost of generation through smarter fuel choices, full utilization of fuel-efficient power plants, and renegotiation of capacity charges with Independent Power Producers (IPPs).

Everyone is aware of the reasons behind the yearly increase in subsidies. Despite a large reserve margin, the power supply chain struggles to meet actual demand. The energy sector fails to meet the requirements of end users. Continuing with a "business as usual" approach makes it highly unlikely that the system can move away from subsidies in the foreseeable future.

Successive governments from 2000 to 2025 are collectively responsible for the evolution of this situation, although most of the damage occurred in the past 15 years. The enactment of the Quick Enhancement of Electricity and Energy Supply (Special Provisions) Act, 2010, and the political vision of "power for all" contributed significantly to the problem. Many large and medium-capacity power plants were built without properly assessing actual demand growth, establishing evacuation infrastructure, or ensuring a consistent primary fuel supply. Numerous contracts with private companies included costly capacity charge provisions. Instead of developing indigenous primary fuel resources, the government opted for imported fuels and power. The COVID-19 pandemic and the Russia–Ukraine war further disrupted global markets.

The government attempted to address the situation by adjusting power tariffs and fuel prices. However, the ongoing energy crisis alone forced many SMEs and medium-sized industries out of business, and most industries are now struggling. Creating a subsidy-free, self-sustaining energy and power sector will be a major challenge for any political party seeking to govern in the next general election.

Way Forward

Experts and observers have been raising concerns and issuing warnings for several years, but these were largely ignored. The interim government has taken some damage control steps by repealing the Quick Enhancement of Electricity and Energy Supply (Special Provisions) Act, 2010, and by restoring the tariff-setting authority to BERC. Outstanding payments in the power and energy sectors have been reduced. However, challenges remain in ensuring a sustainable fuel supply, reducing generation costs, and implementing pricing reforms. Energy efficiency, loss and pilferage elimination, and good governance must be priorities.

The interim government can actively consider the following measures:

- Phase out inefficient plants to lower electricity generation costs and reduce system losses

- Prioritize cheaper fuel sources and diversify the fuel mix for efficiency

- Conduct regular audits to reduce capacity payments to IPPs

- Increase investment in renewable energy to meet the 10% target by 2030

- Align tariffs with production costs while phasing out subsidies by 2026

Several plants in the power system currently consume excessive fuel. Although some fuel-efficient power plants have recently been commissioned, the government must phase out inefficient ones in a structured manner. Once the Rooppur Nuclear Power Plant comes online, Bangladesh will gain a reliable baseload power source, reducing stress on the gas sector. A combination of nuclear, coal, and efficient gas-based plants should meet most of the country's demand, except for short periods during peak summer, when a few liquid fuel-based peaking plants may be required. Otherwise, expensive liquid fuel-based power plants should be retired to reduce overall generation costs.

As far as the fuel mix is concerned, natural gas—both domestic and imported LNG—will continue to dominate until at least 2040. Some voices in Bangladesh suggest avoiding further LNG capacity expansion, but given current realities, this is not feasible. LNG prices are expected to remain manageable over the next 4–5 years, especially if 80% of procurement is secured under long-term contracts. While it's unclear how much domestic gas can be added through expedited exploration, LNG imports will need to increase significantly by 2030.

Bangladesh must prioritize the completion of a land-based LNG terminal at Matarbari by 2030 and consider adding a couple more Floating Storage Regasification Units (FSRUs). LNG will remain a preferred transition fuel globally for the next 10–15 years. Additionally, the country must ensure an uninterrupted coal supply for existing imported coal-based plants. Efforts must also continue to increase hydropower imports from Nepal and Bhutan and to boost renewable energy capacity.

By 2030, we suggest a fuel mix of: Gas & LNG: 40%, Coal: 30%, Imports: 10%, Renewables: 10%, Nuclear: 5%

The government must also review import duties and taxes on solar components such as panels, inverters, and batteries. The power grid must be upgraded to support the evacuation of nuclear and renewable energy.

Energy Efficiency and Transmission Infrastructure

Energy efficiency across the entire power and energy supply chain is key to achieving sustainable energy security. BERC and SREDA must develop the technical expertise to conduct regular energy audits. The government should also review tariffs and capacity charges of IPPs. The plan to promote merchant power plants via Corporate PPAs should be prioritized.

Power transmission and gas transmission are critical areas that require significant attention. Transmission systems must be modernized using advanced technologies. If needed, distributed generation can be adopted as redundancy. The gas transmission grid must also be upgraded to accommodate future LNG imports and gas from onshore and southern fields. A fully operational SCADA system is essential. Many existing transmission facilities, including compressor stations, are underutilized. Improved planning can enhance the utilization of these assets.

We believe that, with proper planning and implementation of the measures outlined above, Bangladesh’s power and energy sectors can become self-sustaining and phase out subsidies by 2030.

Download Special Report As PDF/userfiles/EP_22_24_Special Article.pdf