South Asian countries comprise of 21% of the world's population and 3.8% (US$ 2.9 trillion) of the global economy, as of 2015. South Asia (SA) remains world's fastest growing region with economic growth forecasted to gradually accelerate from 7.1 percent in 2016 to 7.3 percent in 2017. Regional Energy Cooperation in the South Asia Region is on an upward trajectory path particularly in the eastern part of South Asia. Cross Border Electricity/Energy Trade (CBET) and Hydro Power development has gained momentum in last couple of years and also increase in power grids interconnection. Currently CBET is pegged at 2300 MW in SA region. At the highest political level, the region witnessed strong commitment towards Regional Energy Cooperation through signing of SAARC framework agreement on energy cooperation and power trade agreement between India-Nepal. The bilateral frameworks/agreements were further strengthened between India-Bangladesh and India Bhutan for accelerating Energy Cooperation, hydropower development and CBET. Adequate supply of energy is also a pre-requisite for sustaining high economic growth and prosperity in the region. Regional Energy/Electricity Cooperation (REEC) and CBET in SA can significantly address issues of energy security and shortages to a great extent.

Overview of South Asian Power Sector

Per capita electricity consumption (576 KWh/Capita) of SA is one of the lowest in the world whereas world average is around 3000 KWh/capita. To sustain economic growth, electricity demand in the region projected to grow at an average rate of15.2% annually from the period of 2013 to 2040. Currently installed capacity of SA is around 374 GW; (India-330 GW) and projected to be around 1067 GW2by 2040.

Power sector of SA countries are very diverse across their demand pattern, supply source and fuel mix. Afghanistan is a small power system (1341 MW) dominated by hydro and imports electricity. Bhutan is a small power system (1614 MW) dominated by hydro and is the one of the leading exporter of hydroelectricity in the region. Bangladesh with installed capacity of around 15 GW is dominated by natural gas. Bangladesh is facing resource crunch due to the depleting natural gas resources and will remain as one of the leading importer of electricity and energy in future to come. India is the largest power system in the SA region with 330 GW (as on 31.12.2017) of installed capacity dominated by Coal. Long term electricity demand of India is huge and it is the largest market for energy/electricity in the region. Nepal is a very small power system (765 MW) and dominated by hydro power. Country suffers from chronic power and energy deficits and is importing electricity from India. Presently, Nepal is a net importer of electricity from India and in long run can be the exporter of electricity.

South Asia Energy Resources

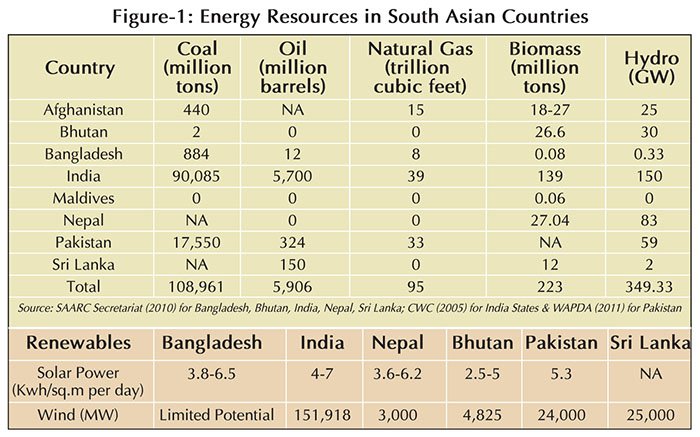

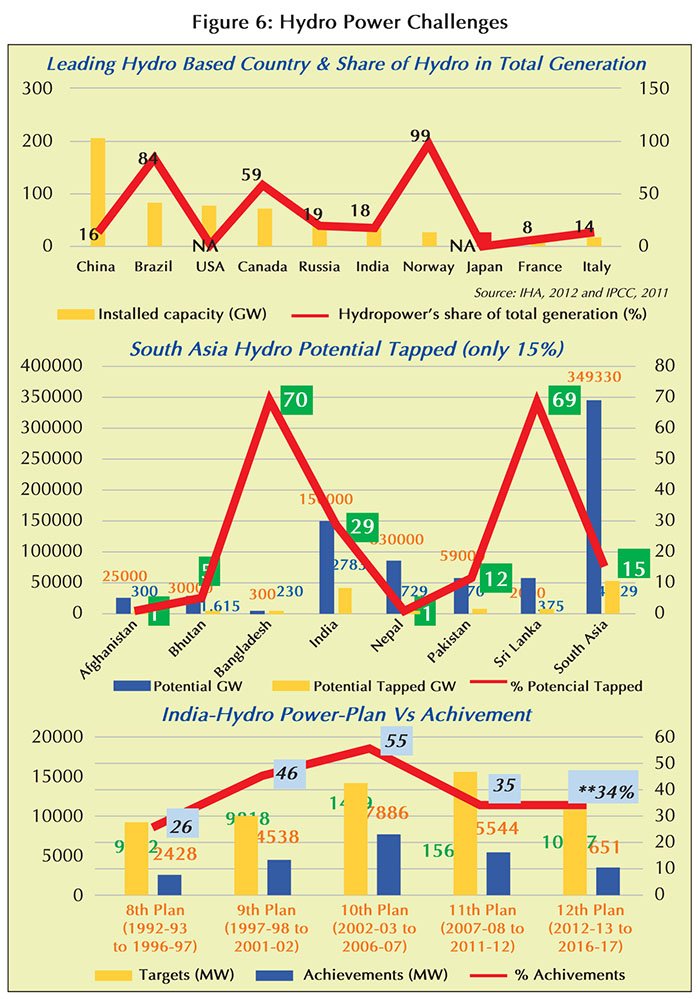

South Asia has huge diversity in energy resources viz. coal, hydro, renewable, natural gas etc. (fig-1). It has limited fossil fuel resources but have substantial hydro energy resources of 350 GW. Energy security has been a concern in the region because growing dependency of oil and gas imports from outside of the region. India & Pakistan are rich on coal and hydro whereas Nepal and Bhutan have only hydro resources. Bangladesh have natural gas resources (natural gas is depleting very fast as its primary fuel source). In South Asia, only 15% of Hydro potential has been developed so far. Nepal and Bhutan have developed 1% and 5% of their hydro potential whereas India has developed 29% of its hydro potential. Sustainable hydropower development needs to be actively pursued in Nepal, Bhutan and India’s north-eastern states which enhance prospects for CBET particularly in the eastern region of SA. There is also a huge potential for solar and wind energy in the region particularly in India, Sri Lanka, and Pakistan.

Existing Regional Cross Border Electricity/Energy Trade (CBET)

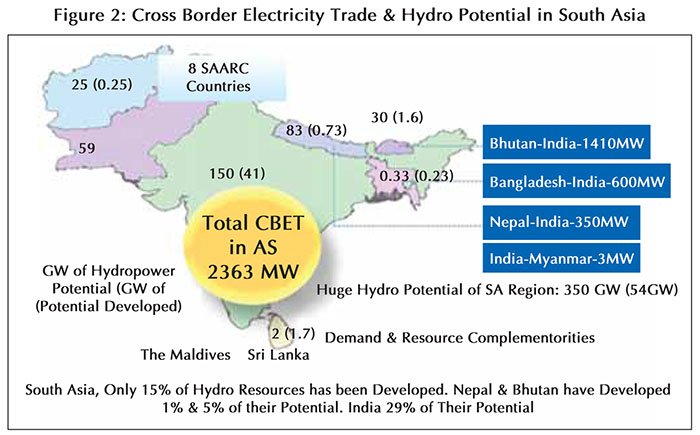

CBET in SA is currently being undertaken between India-Bhutan (~1410 MW), India-Nepal (~310 MW), India-Bangladesh (~600 MW) and India-Myanmar (~3 MW) (Fig-2). Pakistan imports electricity from Iran and Afghanistan imports from Uzbekistan, Tajikistan, etc. The Region is also likely to benefit from Pakistan and Afghanistan’s interconnection with Central Asian countries under the CASA 1000 project. The interconnections between India - Pakistan and India - Sri Lanka are yet to be established, though preliminary feasibility studies have been conducted. India-Bhutan are jointly developing hydropower projects through Intergovernmental and joint ventures. India-Bangladesh are also jointly developing 1320 MW coal fired power project in Bangladesh through Bangladesh-India Friendship Power Company (Pvt.) Limited (BIFPCL). The CBET historically has been mainly through bilateral (Government to Government) arrangements based on case to case negotiations, though in the recent past market-based CBET began between India-Bhutan and India-Bangladesh. It is expected that going in future the CBET in south Asia will be more of market oriented. The political climate is becoming increasingly more and more conducive for CBET both at the bilateral and as well as at the multilateral level as eight-member states of South Asian Association for Regional Cooperation3(SAARC) countries signed SAARC Framework Agreement of Energy (Electricity) Cooperation. Further, the historic Power Trade Agreement (PTA) signed between India-Nepal, opens up a whole range of new possibility for trade electricity between Nepal-India, and also gives an access to Nepal power developers to Indian power market. SA countries are pursing regional energy cooperation through intergovernmental regional forums such as SAARC, BBIN4 framework and The Bay of Bengal Initiative for Multi-Sectoral Technical and Economic Cooperation5 (BIMSTEC). Moving from bilateral trade, India-Bangladesh-Bhutan trilateral Initiative for CBET is expected to happen in near future for Cooperation in the field of Hydroelectric Power6.

Benefits of Existing Regional Cross Border Electricity/Energy Trade (CBET)

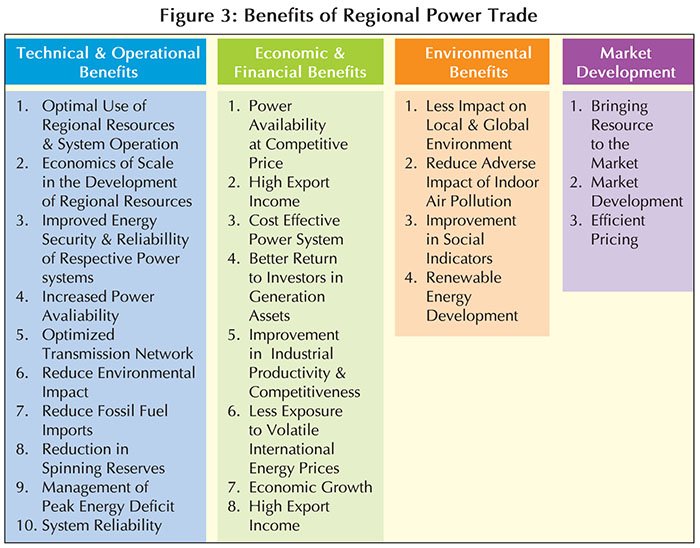

Existing power trade in the region have shown win-win situations/benefits (fig-3) for all the South Asian Countries for creating strong conditions for accelerating/advancing CBET in the region. For example, Hydropower exports (only surplus) to India provided more than 40% of Bhutan’s revenues7 and constitute 25% of its GDP which helped increasing electricity access (95% of population electrified), creating industries like cement and steel etc. Further export of 500 MW8 power from India to Bangladesh has helped in reduction in load shedding (1048 MW of load shedding in 2012-13 to 307 MW of load shedding in 2014-15) and has helped Bangladesh estimated annual savings for Bangladesh is around Taka9 40 billion (US$500 million approx.) (Shahi 2014). On other hand, India being net exporter of electricity, is benefiting from optima utilization of generation assets and revenue earrings.

Key Drivers for CBET in SA

Policy makers in SA recognize the importance of electricity/energy for achieving economic and developmental objective of the region. Key drivers for accelerating CBET in the SA region are

• Low per capita electricity consumptions

• Electricity shortages, poor access to electricity

• Optimal utilization of energy resources

• Dependency on fossil fuel imports

• Diversification of generation mix

• Power availability at competitive price

• Avoided generation capacity

• Sustainable clean energy development

• Synergies in regional emery/power system development and operation

• Energy Cost Saving

A modelling study conducted by World Bank10shows that the regional electricity cooperation and trade could reduce total undiscounted electricity supply costs in the region by US$222 billion, or more than US$9 billion per year over the time period studied (2015-2040). Demand and supply diversity among SA countries, Seasonal complementarities, different time zones, holiday’s pattern are also the key drivers for promoting CBET in the most optimal manner.

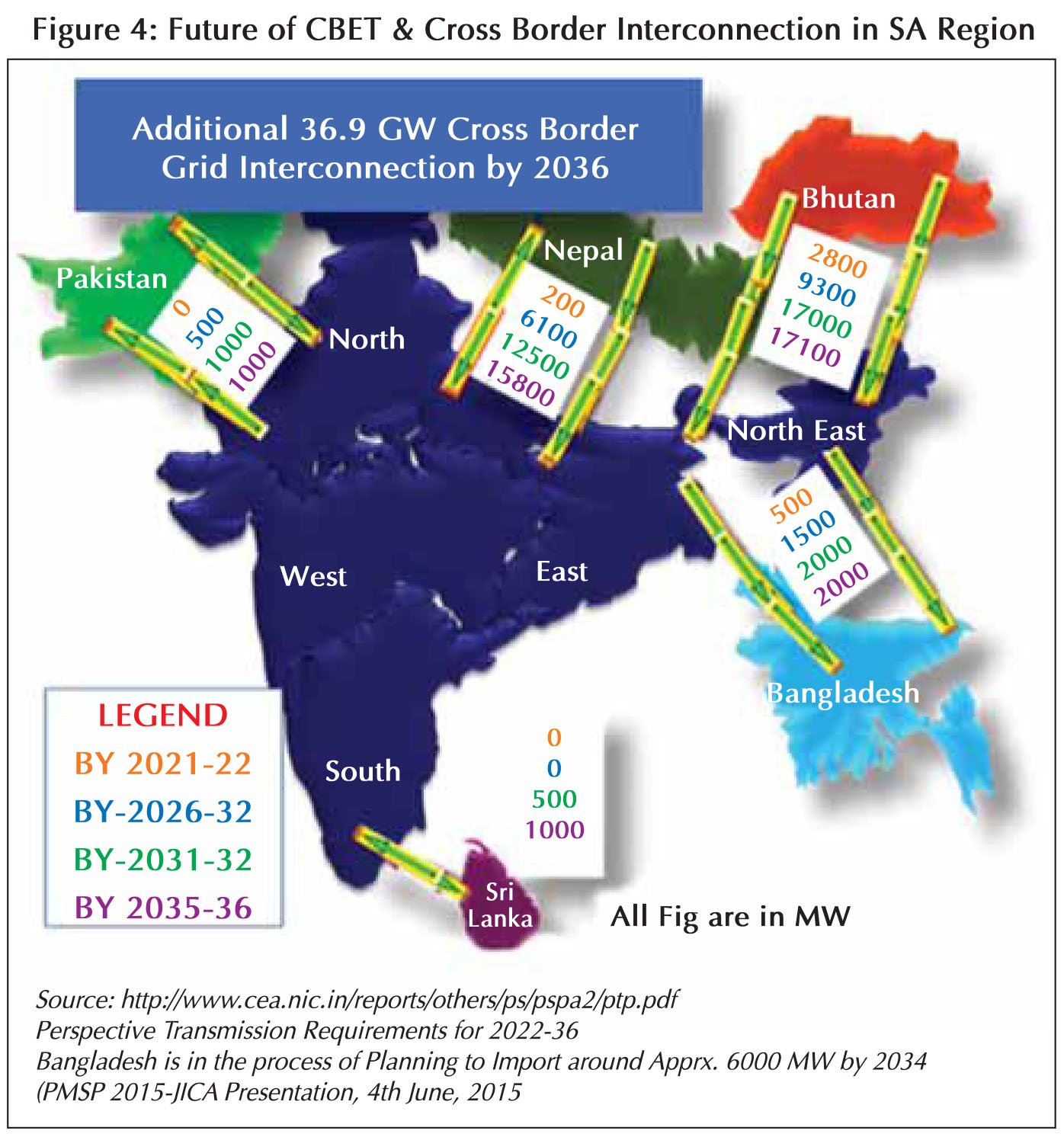

Future of CBET & Cross Border Interconnection in SA Region

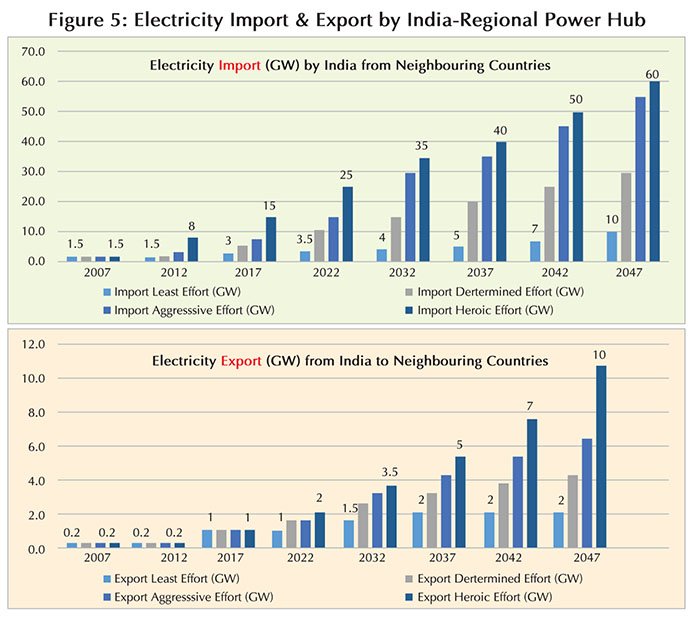

Recognizing the benefits of power trade, all the south Asian countries are taking significant steps to deepen regional energy cooperation and advance CBET. India having large power system is centrally located in the region and poised to be regional energy and power hub in the region. To enhance CBET, significant high voltage cross border interconnections of 36.9 GW (fig-4) are being planned and proposed in the region, as per the perspective transmission requirements for 2022-3611 developed by Central Electricity Authority, India. Bangladesh in its power system master plan-2016 also intends to import around 8500 MW from its neighboring countries including 500 MW of hydro power from Myanmar by 2040. As per NITI Aayog of India, electricity Import (GW) from neighboring countries could be in the range of 10 GW to 60 GW and electricity export of 2 GW to 10 GW by 2047 in the different scenarios(fig-5). On energy trade front, there are plans to build oil pipeline between India-Nepal i.e. Raxaul-Amlekhgunj oil pipelines and also to extend liquefied petroleum gas (LPG) pipeline up to Nepal’s border at Amlekhgunj. India also plans to build pipelines to carry diesel and natural gas to Bangladesh. A 131-km pipeline proposed to be laid from Siliguri in West Bengal to Parbatipur in northern Bangladesh to transport diesel, and a line from Dattapulia in West Bengal will take natural gas to Khulna, the third-largest city of Bangladesh. India’s Oil and Natural Gas Company (ONGC) and Bangladesh Petroleum Corporation (BPC) are in negotiation to build the 6,900-km long gas pipeline as envisaged in the hydrocarbon vision 2030 that will be linking Bangladesh, Myanmar and north-eastern states12. India’s northeast region, already is a net exporter of petroleum products and excess capacity can service demand in neighboring nations such as Bangladesh, Myanmar, Sri Lanka and Bhutan. Pipeline Corridor between Bangladesh and India for Crude Oil Imports and Product Supply will be beneficial to both countries. Bhutan and Nepal present export opportunities to replace fossil fuel by cleaner sources of energy, i.e. hydro power.

Investment Requirements

As per the world bank estimation, South Asian countries needs an investment13 of USD 1.7 to 2.5 trillion (2011-2020) to bring its power, roads, water supplies up to the acceptable standard needed to serve its population. Out of above, an investment of USD 632 billion will be required for electricity infrastructure development. Bangladesh, India, Nepal, Pakistan and Sri Lanka are expected to invest around US$16.5 Billion, US$ 468.8 Billion, US$7billion, US$ 96 Billion and US $ 9 Billion respectively by 2020 for the electricity infrastructure development. For an integrated regional power grid, South Asia is projected to need at least USD 1,390 billion for expanding electricity generation from 2015 to 2040 period (in order to add approximately 750 GW of electricity generation capacity).

Challenges associated with development of Hydro Power

Sustainable development of hydropower power potential has not been easy. Globally, around14 19% of the hydro power potential has been developed so far. In south Asia, only ~15% (Fig-615) of the hydro resources has been developed so far. Nepal and Bhutan have developed 1% and 5% of their hydro potential whereas India has been able to develop 29% of its hydro potential. Hydro power development has been impacted/delayed as huge risks are associated with hydropower such as a) geological uncertainties/natural calamities b) land acquisition /environment and forest issues c) rehabilitation & resettlement /law & order problem & local issues d) difficult terrain, poor accessibility e) investment and financing) long gestation period etc. While there are challenges associated with development of hydropower, considering the advantages/benefits of hydropower such as clean & renewable source, helps in reduction of CO2 emission, load balancing, fuel at zero cost, easy operation etc. and therefore there is need to peruse development of hydropower.

Risks and Challenges for Accelerating Cross Border Electricity Trade in South Asia

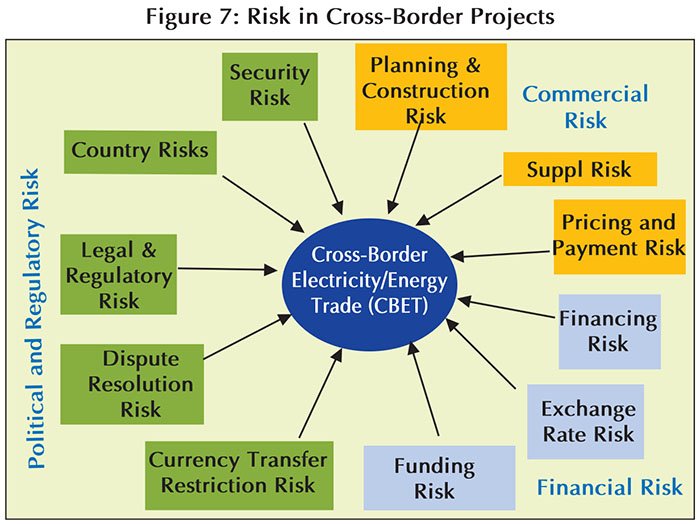

Lack of common set of policy, legal, and regulatory frameworks, political commitments, inadequate transmission system interconnections and lack of regional electricity market creates various risks and challenges (fig-716) for accelerating CBET in South Asia Region. Further, the cross-border element tends to increase the risks associated with project implementation. Hence, risk identification and balanced mitigation is important for promoting investment and CBET in the Region.

International Experience/Best Practice for promoting investment

Keeping in view of the potential risks involved in development of hydro power & investment both in domestic and CBET projects, SARI/EI/IRADe undertook the study of international power pools which can provide learnings in terms of best practices and practical approaches for the South Asia region. The ongoing trade in power pools like SAPP, GMS, ASEAN Power Grid, Gulf Cooperation Council (GCC) countries, West African Power Pool (WAPP), cross border trade between Georgia-Turkey etc. are relevant examples of CBET for South Asia. The study shows that initially the investments in CBET projects can be done on a bilateral basis, but it eventually needs to be evolved under a regional body, which is responsible for the identification of CBET projects, and also determine terms of selection and award through the private sector or MFI route. These decisions have to be supported through a regional framework and guidelines. The following lessons/learning from the international review were.

• Inter-governmental Agreements and Multilateral MoUs: Inter-governmental agreements would help to protect and reduce the risks of policy/regulatory surprises and expropriation.

• Competitive Market Pricing: Setting up a competitive market pricing mechanism is important in reducing potential pricing risk in power projects and CBET.

• Commercial Arrangements: Need to have standard contracts that fully incorporate the consequences of contractual defaults and emergency events.

• Exploring the funding from the International Financial Institutions (IFIs), Multilateral Development Banks for concessional debt financing and technical assistance etc.

• Dispute Resolution: Dispute resolution through transparent settlement procedures, standard PPAs, Regional/International arbitration etc.

• Coordinated Planning and Implementation: Need to have regional planning and master plan implemented through regional coordination technical agency.

• Guarantee against Nationalization: Political insecurity is the main concern of foreign investors. Having guarantees against such risk would improve the investor’s comfort and confidence.

International experience shows that the financing of CBET power projects faces many difficulties due to the involvement of various governments leading to a mismatch in the frameworks, uncertainties in policy and regulatory frameworks, etc. Thus, it is important to have a regional coordinating institutional mechanism to provide investors some comfort by way of regional planning and selecting regional projects with the consent of the majority of member countries of the coordination body. This reduces the revenue risk of the project and also keeps in check the potential of any arbitrary decisions being taken by the stakeholder.

Way Forward/Key Recommendations for Accelerating Investment & CBET in South Asia

Based on the review of policy and regulatory frameworks prevailing in the SA region and also drawing international experience, suggested Way forward/Recommendations for accelerating investment and Cross Border Electricity Trade in South Asia Region are as follows:

a) Political/Country Risk: There are various Political/Country risk associated with Investment in CBET Projects such as unilateral changes in agreement, Change of Law and social unrest etc. There is a need to have Strong regulatory enforcement, to insulate business operations from political risks/decisions. To cover these risks, the various instruments available are i) International investment agreements (Bilateral investment treaties, Free trade agreements, MOUs, Host government Agreements- HGAs etc.) ii) Political insurances, iii) Guarantee against expropriation without compensation iv) sovereign guarantees, MIGA guarantees etc.

b) Policy, Regulatory and Legal Risks: Policy, regulatory and legal framework differs in each SA country, which increases the risk of promoting investment and CBET in the region. Lack of legal framework, common set of policies and regulations, contractual enforcement, transparent dispute resolution mechanism increases risk of investment. Common set of harmonized/coordinated regional policy, regulatory and legal framework should include a) formation of institution/association /forum of regulatory body for cross cutting of regulations, recognition of CBET/Trade in the national policy & laws b) Open access to transmission network c) licensing for power trade d) imbalance settlement mechanism e) coordinated transmission planning and procedures for integrated system operation f) Harmonization of technical standards and grid Codes g) Dispute resolution Mechanism including arbitration provisions. Further, the followings are suggested to promote investment in the region:

• Regional investment policies for frictionless flow of investment, skilled labor, technology & other resources, protection of property right etc.

• Regional trade policy to address various issues e.g. project development & operation, technology transfer etc., to reduce transaction cost.

• National competition policy in consistence with regional investment policies, to promote regional investment.

• Promotion of public investment in energy project through BOO, and BOOT business models under PPP.

• A credit rating framework at the regional level could be considered for the utilities in the region to provide guidance to international investors.

c) Off-take risk: Considering concerns of developers, lenders, following is recommended to mitigate the risks vis-a-vis to promote investment:

• Bankable contractual agreements like Power Purchase Agreements (PPAs), Transmission Service Agreements (TSAs), which have provisions of compensation in the PPAs, pass through of cost etc.

• Guidelines on the foreign currency denominated PPAs for CBET projects should be specified at the country level and to be consistent with principles evolved at the regional level.

d) Payment and Project Development Risk: Developer’s Risk mitigation through appropriate payment security mechanisms, the local processes for the approvals and clearances need to be streamlined and made investor friendly for CBET projects.

• Suitable/secured Payment Security Mechanism such as irrevocable Letter of credit, sovereign guarantee, bank Guarantee, escrow account etc.

• Standard technology specific project development guidelines to promote regional investment

• Regional Coordinating body may be formed to address proposal relating to CBET projects.

• Countries should facilitate in land acquisition and related issues

• Single window clearance for regional investment projects

• Regional skill development center.

e) Taxation policy Risk:

The taxation policies impact investment in CBET projects. South Asian Countries need to have a) Nondiscriminatory tax policy for regional investor b) consistent and stable tax regime and c) Simplification of taxes for import and export duty for regional trade etc.

f) Financing:

Power Projects being capital intensive, arranging cheaper source of funding, innovative financing and financial closure of the projects are challenge. South Asian Countries can promote and facilitate for Green funding options (e.g. green bonds, clean tech funds), develop comprehensive financing ecosystem (exchange, platform, broker, market-makers, advisor, equity research etc.), work towards integration of capital market and prioritizing of cross border power projects (especially clean energy project) and economic incentives for the promotion.

g) Corporate Governance: Better corporate governance facilitates investment and there is a need to have Disclosure requirements, Uniform accounting, auditing principals, reporting standard for investors etc.

h) Currency fluctuation risk: Volatility in exchange rate, Currency convertibility risk and Expatriation affects the CBET projects and investment. SA countries need to have Consistent currency flow regulation, PPAs in acceptable denominated and provision for Mitigating the currency hedging risk and reducing the cost of capital.

i) Market Development: Development of Regional power market is critical for sustaining CBET and development of hydro power resource there by addressing various markets/commercial risks in the South Asia Region. It will also help to capture non-energy benefits of hydropower and thereby increasing the long term commercial viability of CBET and hydro power projects. A vibrant South Asian Regional Power Market will make CBET competitive and create a fair and transparent and commercial pricing mechanism framework which in turn, will streamline investment, making it lucrative for investors who seek fair, steady and risk mitigated short and long term returns on their capital.

V. K. Kharbanda;

Project Director, IRADe

Rajiv Ratna Panda;

Head-Technical, SARI/EI, IRADe, India

Email: rajivpanda@irade.org ,rajivratnapanda@irade.org

Reference:

1.World Bank Policy Research Working Paper 7341, How Much Could South Asia Benefit from Regional Electricity Cooperation and Trade? http://documents.worldbank.org/curated/en/846141468001468272/pdf/WPS7341.pdf

2. World Bank Policy Research Working Paper 7341, How Much Could South Asia Benefit from Regional Electricity Cooperation and Trade? http://documents.worldbank.org/curated/en/846141468001468272/pdf/WPS7341.pdf

3. South Asian Association for Regional Cooperation (SAARC) consists of Afghanistan, Bangladesh, Bhutan, India, Nepal, the Maldives, Pakistan and Sri Lanka.

4. The Bangladesh, Bhutan, India, Nepal (BBIN) Initiative is a sub-regional architecture of countries in Eastern South Asia, a sub region of South Asia. It meets through official representation of member states to formulate, implement and review quadrilateral agreements across areas such as water resources management, connectivity of power, transport, and infrastructure.

5. The Bay of Bengal Initiative for Multi-Sectoral Technical and Economic Cooperation (BIMSTEC) is an international organization involving a group of countries in South Asia and South-East Asia consisting of Bangladesh, India, Myanmar, Sri Lanka, Thailand, Bhutan and Nepal.

6. India - Bangladesh Joint Statement April 08, 2017

7.http://www.oecd.org/countries/bhutan/48651659.pdf

8. India-Bangladesh power trade started on 5th October, 2013

9. http://www.ideasforindia.in/article.aspx?article_id=1589

10. How Much Could South Asia Benefit from Regional Electricity Cooperation and Trade? World Bank Group policy research working paper 7341, June 2015

11. http://www.cea.nic.in/reports/others/ps/pspa2/ptp.pdf

12. http://www.newindianexpress.com/nation/2017/jan/23/india-bangladesh-negotiate-gas-pipeline-1562721.html

14.http://www.iea.org/publications/freepublications/publication/hydropower_essentials.pdf

15. https://sari-energy.org/wp-content/uploads/2016/09/Brief-Report-on-SARI-EI-Participation-in-the-Myanmar-Green-Energy-Summit-15th-16th-August2016-Yangon-Rajiv-1.pdf

16. 6https://sari-energy.org/wp-content/uploads/2016/09/Brief-Report-on-SARI-EI-Participation-in-the-Myanmar-Green-Energy-Summit-15th-16th-August2016-Yangon-Rajiv-1.pdf