Prelude

Bangladesh’s power sector is grappling with a wide range of challenges despite sustained government investments intended to build domestic and foreign confidence. The problems span delayed bill payments, rising subsidies, tariff gaps, liquidated damage deductions, surplus generation capacity, contractual obligations, and more. Although infrastructure has expanded significantly and subsidies have surged, the country continues to face inefficiencies and mounting arrears that now threaten the sector’s long-term sustainability.

Escalating Subsidies

The Bangladesh Power Development Board (BPDB) purchases electricity at high cost and sells it at lower regulated prices, requiring substantial government subsidies to cover the shortfall. Despite expanded generation capacity, Bangladesh remains heavily dependent on imported fuel, driving up production costs.

Over the last five fiscal years, the country has spent roughly Tk 1.474 trillion in subsidies. Between FY 2020–21 and FY 2023–24 alone, subsidies totaled Tk 854.11 billion, and the revised FY 2024–25 allocation represents an all-time high. From FY 2020–21 to FY 2024–25, electricity subsidies have increased by nearly 700%. (Table 1)

.jpg)

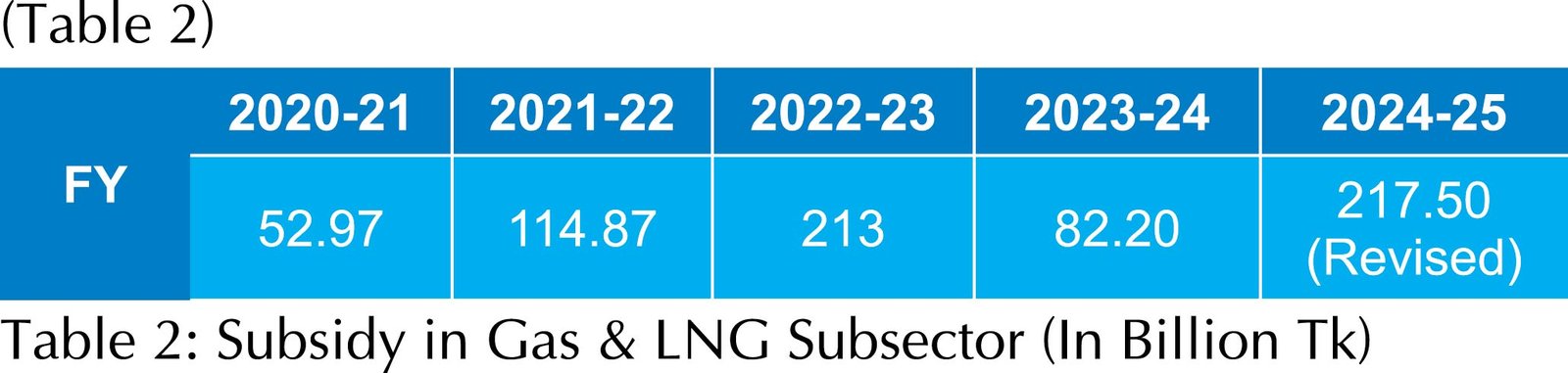

In the same five-year period, subsidies to the gas and LNG subsectors totaled Tk 680.54 billion, marking a 400% rise. (Table 2)

The core driver is Bangladesh’s reliance on costly imported LNG, sold domestically at much lower rates. For example, Petrobangla’s supply cost per cubic meter (NG + LNG) is Tk 29.39, while consumers pay only Tk 22.87, creating a significant revenue gap that subsidies must fill.

Unpaid gas bills further exacerbate fiscal stress. As of February 2025, industrial sectors owed more than Tk 210 billion to six major gas distribution companies. (Table 3)

Total arrears are expected to exceed Tk 230 billion once the March-April 2025 dues are counted. Despite this spending surge, the sector continues to suffer from deep inefficiencies, primarily due to rising costs associated with imported fuel and idle generation capacity.

Reducing subsidies would have mixed effects, likely raising short-term inflation but improving fiscal stability, encouraging efficiency, and enabling targeted support for low-income households. Higher tariffs could also push consumers toward more efficient energy use and accelerate the adoption of renewable energy.

The budgetary savings can be redirected into targeted social safety net programs to support vulnerable low-income families. This is more efficient than universal subsidies that disproportionately benefit high-income consumers. Higher electricity prices encourage more efficient energy use, discourage overuse and wastage often associated with underpriced energy. Even by making conventional energy sources expensive, limited subsidies can encourage the development and adoption of renewable energy sources (solar and wind energy), contributing to a diversified and sustainable energy mix. In essence, reducing subsidies with careful policy design, management, monitoring, and targeted support can lead to an efficient, financially stable, and sustainable power sector and national economy.

Capacity and Challenges in Electricity Generation

Under the Power System Master Plan, electricity generation capacity was increased from 22,031 MW in FY 2020-21 to 28,998 MW within FY 2024-25. The maximum power generation shows 16,477 MW at present. Here, electricity demand failed to keep pace, resulting in surplus capacity and idle plants, which still required capacity payments. From FY 2020-21 to FY 2023-24, the capacity charges paid by BPDB for private and rental power plants were: Tk 132 billion in FY 2020-21, Tk 240 billion in FY 2021-22, Tk 260 billion in FY 2022-23, and Tk 320 billion in FY 2023-24. The capacity charge for private producers is Tk 380 billion in FY 2024-25. (Table 4)

Electricity Generation versus Selling Cost (Tariff)

The BPDB's annual report for 2022-23 indicated per unit (kWh) average bulk production cost of electricity was Tk 11.33, while the average selling price remained at Tk 6.70, resulting in a loss of Tk 4.63 per kWh. This imbalance is a significant factor contributing to the BPDB's financial losses. Later in March 2024, the average bulk-level electricity tariff increased to Tk 7.04/unit (USD 0.058/unit) from Tk 6.70/unit. This disparity is still attributed to factors like the increasing cost of private sector power generation and the need to maintain lower selling rates for consumers.

In India, the selling price of electricity is generally higher than the purchase rate, though both can vary significantly. The purchase rate specifically for solar power can be lower, while the selling rate to consumers can range up to ₹ 8.00 (USD 0.09) per kWh (according to NoBroker). Factors like usage, electricity providers, and government subsidies influence the rates, with different rates for residential, commercial, and industrial consumers.

In Pakistan, power purchase rates for grid-connected solar systems are significantly lower than the selling price for grid electricity. Under the revised policy, power companies purchase surplus solar electricity at Rs 10.00 per unit (kWh), while selling grid electricity at Rs 42.00 (USD 0.15) per kWh during off-peak hours and Rs 48.00 (USD 0.17) per kWh during peak hours, excluding taxes. This difference incentivizes consumers to self-consume more of their solar-generated electricity and reduce their reliance on the grid during peak hours.

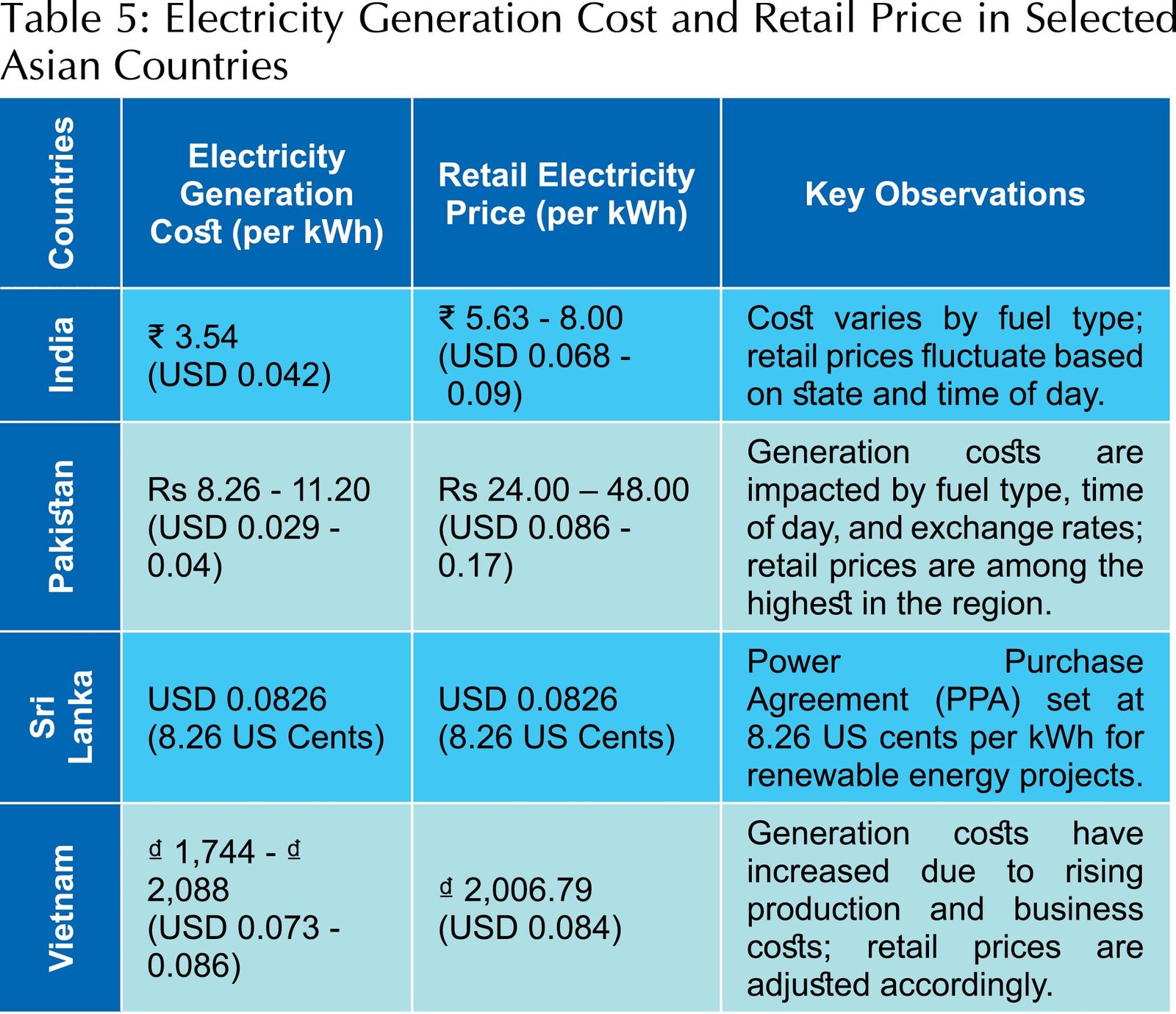

In general, the electricity generation and retail cost (excluding VAT) in some of the Asian countries in 2023 is shown in the next table. (Table 5)

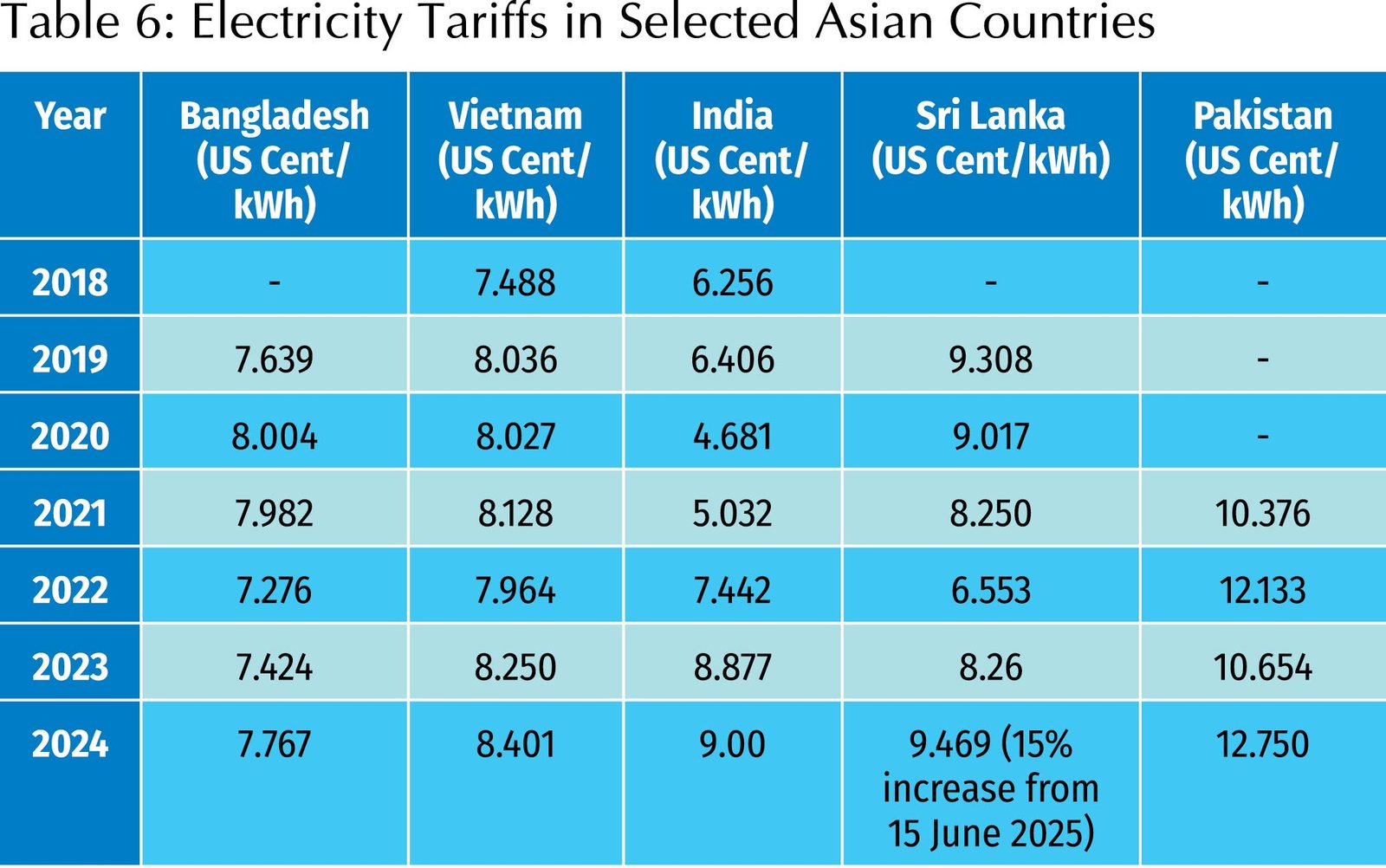

The historical Electricity Tariff (excluding VAT) Variation of some of the Asian countries, including Bangladesh, varies (US Cent/kWh) from 2018-24 as shown in Table 6.

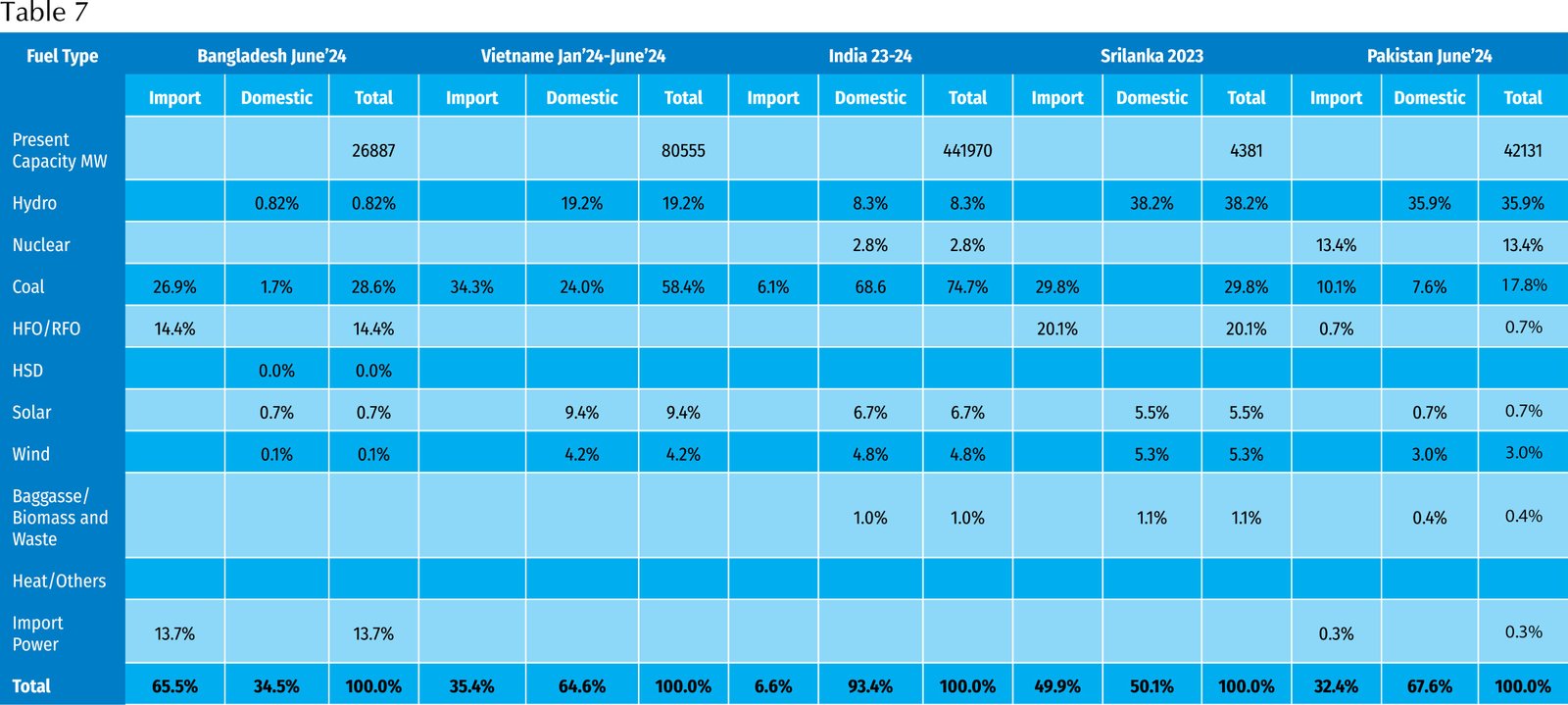

The cost of generating electricity also varies significantly with the usage of fuels and the sources of supply. Different types of fuels (imported with higher cost and domestically sourced with comparatively lower cost) used for generating electricity in neighboring countries are shown in the following: (Table 7)

Comparing the above tables, Bangladesh maintains the lowest tariff despite being the largest importer of primary fuel for electricity generation. This phenomenon has continued to decline over the years- a trend that raises concerns about long-term financial sustainability.

Payment and Circular Debt

The BPDB has a huge backlog of unpaid bills to Independent Power Producers (IPPs), which mounted at approximately Tk 200 billion (or Tk 20,000 crore) as of late October 2025. This situation is causing severe financial stress for IPP operators, impacting their ability to import fuel, pay debts, and maintain their plants. The Government has been considering issuing bonds to clear these debts. However, the BPDB's payments to IPPs have increased considerably from FY 2021 to FY 2025, which is driven by capacity charges, increased power demand, and the impact of fluctuating exchange rates. These have led to a significant increase in Government subsidies to cover these costs and ensure the availability of electricity to the national grid.

The core issue stems from a circular debt cycle, which leaves everyone indebted, resulting in a growing debt spiral. Power plants generate electricity using gas, but are not paid on time by BPDB. As a result, they are unable to pay gas distribution companies, which hampers the IPPs’ ability to operate and maintain infrastructure. Even though the government has made some progress in reducing arrears to IPPs, payments to gas companies remain sluggish. The service charge cut from 9% to 5% for importing Heavy Fuel Oil (HFO), implemented unilaterally by the BPDB, has also generated friction with IPPs.

Deduction as Liquidated Damage (LD) Against Submitted Invoices of IPPs

The issue of deduction as LD from the Capacity Payment on account of alleged outages against the submitted invoices for the supply of electricity has become a growing concern for the IPPs. The BPDB has suspended the right to dispatch the Facility under clause 13.2 (j), under the PPA with IPPs.

Notification of Net Energy Output Demand.

It is critical to have timely and prudent notification of Net Energy Output demand by the BPDB as per the PPA. The absences of forecasting demand adversely impact IPPs’ ability to efficiently fulfil the contractual obligations. As per PPA Section 9.3 (a, b, c, d), the BPDB is required to provide estimated requirements or demand for Net Energy Output during a contract year in the following manner.

Year Ahead Notification: Not less than ninety (90) days before the beginning of each Contract Year, BPDB shall provide to the company estimated requirements monthly, for the Net Energy Output during that contract year.

Quarter-ahead Notification: Not less than sixty (60) days before each Contract Year quarter, BPDB shall provide the company with estimated requirements on a week-by-week basis for Net Energy Output and maximum capacity during that quarter.

Month-ahead Notification: Not less than fourteen (14) days before each Month, BPDB shall provide the company with estimated requirements on a Day-by-Day basis, for Net Energy Output and maximum capacity required during that month.

Week-ahead Notification: Not less than forty-eight (48) hours before each Week, BPDB shall provide to the company estimated requirements, on an hour-by-hour basis, for Net Energy Output and maximum capacity during that week.

These notifications are vital for IPP to accurately plan the budget, operations, fuel procurement, and financial management. Unfortunately, the absence of such notifications by the BPDB has caused significant disruptions:

Operational Challenges: Mismatches between demand and supply have led to frequent situations of overstock or shortages of Heavy Fuel Oil (HFO). This requirement has further complicated fuel procurement for the plant. In such a case, if BPDB does not adhere to the PPA guidelines regarding Net Energy Output demand, it will lead to increased operational costs.

Financial Strain: HFO storage for a long time, which leads to higher costs for fuel procurement and financial losses due to inappropriate resource allocation. The inability to align operational plans with accurate demand projections has further stressed IPPs’ financial management.

Such disruptions hinder IPPs’ ability to forecast actual demand from the National Load Dispatch Centre (NLDC) and negatively impact long-term planning for operations, fuel procurement, and financial strategies.

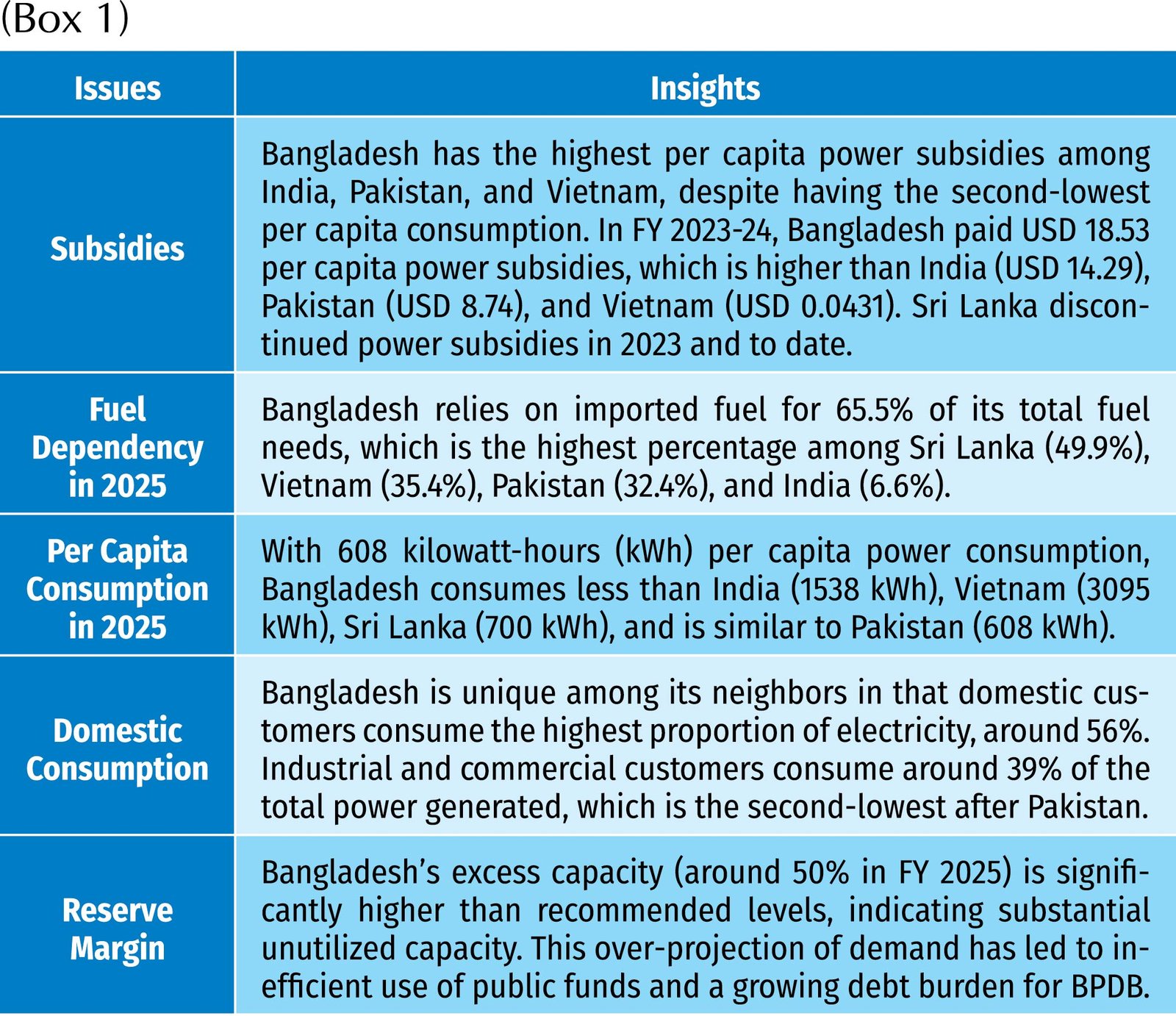

Insights Comparing Bangladesh's Power Sector to Other Asian Countries

Bangladesh's power sector faces significant inefficiencies and overcapacity compared to other Asian countries. Here, generation capacity has increased, and demand has not kept pace, leading to surplus capacity. Idle plants that still require capacity payments and government subsidies. The BPDB also purchases electricity at higher costs and sells it at subsidized rates, creating a persistent financial gap. The construction of numerous rental and quick rental plants since 2010 has also incurred substantial costs. Experts note that Bangladesh's power generation capacity exceeds demand by 45%, significantly more than the optimal 8-10%. (Box 1)

Government Response and Structural Challenges

In response to mounting unpaid bills and subsidies, the Energy Division under the Ministry has adopted stricter measures:

- Disconnection of gas supply for defaulters with more than two months of arrears.

- Deployment of magistrates to dismantle illegal connections.

- Formation of committees to resolve outstanding bills, especially from government entities.

Energy Adviser Dr. Muhammad Fouzul Kabir Khan has emphasized the need to shift towards locally-sourced, cost-effective energy and reduce fiscal burdens caused by excessive reliance on imports. However, the implementation of domestic gas exploration projects remains slow. Stakeholders, including David Hasanat, President of Bangladesh Independent Power Producers’ Association (BIPPA), have acclaimed recent improvements in Government payment schedules, but cautioned that inconsistent policy decisions could destabilize investor confidence.

Despite these actions, long-term sustainability remains in question. Experts argue that overreliance on LNG imports, failure to explore and develop domestic gas reserves, and poor financial management have made the sector increasingly unsustainable.

Conclusion

Bangladesh’s power sector stands at a critical juncture. Rising subsidies, misaligned capacity expansion, and a deepening debt cycle threaten long-term energy security. Only bold, comprehensive structural reforms—focused on domestic resource development, realistic demand planning, and timely financial settlements—can restore stability and build a sustainable future for the sector.

Colonel (Retd) Engineer A R Mohammad Parvez Mazumder, afwc, psc

Download Analysis As PDF/userfiles/EP_23_12_Analysis.pdf