Bangladesh enters 2026 with a power-sector contradiction that is becoming harder to ignore. The country still depends significantly on imported fuels, remains exposed to global commodity shocks, and continues to carry the economic memory of tariff pressure and periodic load shedding. At the same time, the government has announced an ambitious new direction: securing 10,000 megawatts of electricity from renewable sources by 2030.

At first glance, the announcement sounds like a conventional policy target. But it is more consequential than that. It reflects a growing recognition that the old electricity model, while useful in an earlier phase of development, is becoming costlier, riskier, and less compatible with the next stage of Bangladesh’s economic ambitions.

The country’s previous power strategy was built around urgency. Demand was rising rapidly. Factories needed electricity. Cities were expanding. Households expected better service. In that context, quick additions through gas generation, rental plants, liquid-fuel units, imported LNG, and coal projects were understandable responses to genuine shortages. That approach helped Bangladesh reduce blackouts and support industrial growth.

But what solved yesterday’s supply problem has increasingly created today’s affordability and vulnerability problem.

Recent global energy disruptions have clearly exposed those weaknesses. Oil prices surged. LNG markets became volatile. Shipping costs rose. Exchange-rate pressure intensified. Subsidy burdens expanded. Businesses struggled with cost uncertainty. Consumers faced higher tariffs directly or indirectly. Even when the immediate stress eased, one structural lesson remained: a growing economy cannot indefinitely rely on expensive, externally priced fuels as the backbone of energy security.

That is why the renewable target matters. It is not merely a climate promise or diplomatic slogan. It is an economic strategy.

Still, announcements alone do not generate power. Targets do not install turbines. Policy statements do not build substations, secure land, attract investors, or modernize transmission systems.

So, the central question must be asked honestly: Can Bangladesh really reach 10,000 MW by 2030? The realistic answer is yes, but only under conditions of unusual administrative seriousness. If 2026 and 2027 become years of disciplined execution, Bangladesh can move surprisingly far. If they become years of speeches, committees, and procedural delays, the target will slowly fade into symbolism.

Why is the old energy model under pressure?

Bangladesh’s traditional power strategy relied on a combination of domestic gas, emergency generation, and, later, imported fuels. That model had practical logic. Domestic gas was once relatively cheap. Rental plants added capacity quickly. LNG imports were expected to supplement declining gas fields. Imported coal was considered a source of baseload power. But over time, five structural weaknesses became harder to ignore:

1. Dependence on external fuel prices―When global oil or gas prices rise sharply, Bangladesh’s generation cost also rises.

2. Pressure on foreign exchange reserves―Fuel imports require dollars. During reserve stress, power security becomes linked to macroeconomic management.

3. Tariff and subsidy tension―Higher costs must eventually be borne by consumers, taxpayers, or both.

4. Supply Vulnerability―Wars, shipping disruptions, or commodity shocks abroad can create stress at home.

5. Industrial competitiveness risk―Manufacturing economies require reliable and reasonably priced electricity. Uncertain costs weaken competitiveness over time.

Renewable energy cannot eliminate every challenge. But solar and wind plants do not require continuous import of fuel oil once commissioned. Their long-term economics depend more on capital cost, financing conditions, and system integration than on volatile commodity prices. For Bangladesh, renewables are therefore no longer only an environmental preference. They are increasingly an economic stabilization tool.

Why does 10,000 MW matter now?

Some targets are symbolic. This one is strategic. If implemented seriously, 10,000 MW of renewable electricity could help Bangladesh:

- reduce dependence on imported liquid fuel generation

- diversify the national power mix

- lower long-term exposure to commodity shocks

- improve reserve management by reducing fuel import demand

- attract green finance and development support

- strengthen export competitiveness through cleaner supply chains

- create domestic technical employment

There is also an important trade dimension. Global buyers increasingly examine carbon footprints, sustainability metrics, and energy sourcing practices. For Bangladesh’s export industries, especially garments and manufacturing, access to cleaner power may gradually become a commercial advantage. That means renewable energy policy is not only about climate. It is also about industrial strategy.

Where does Bangladesh stand today?

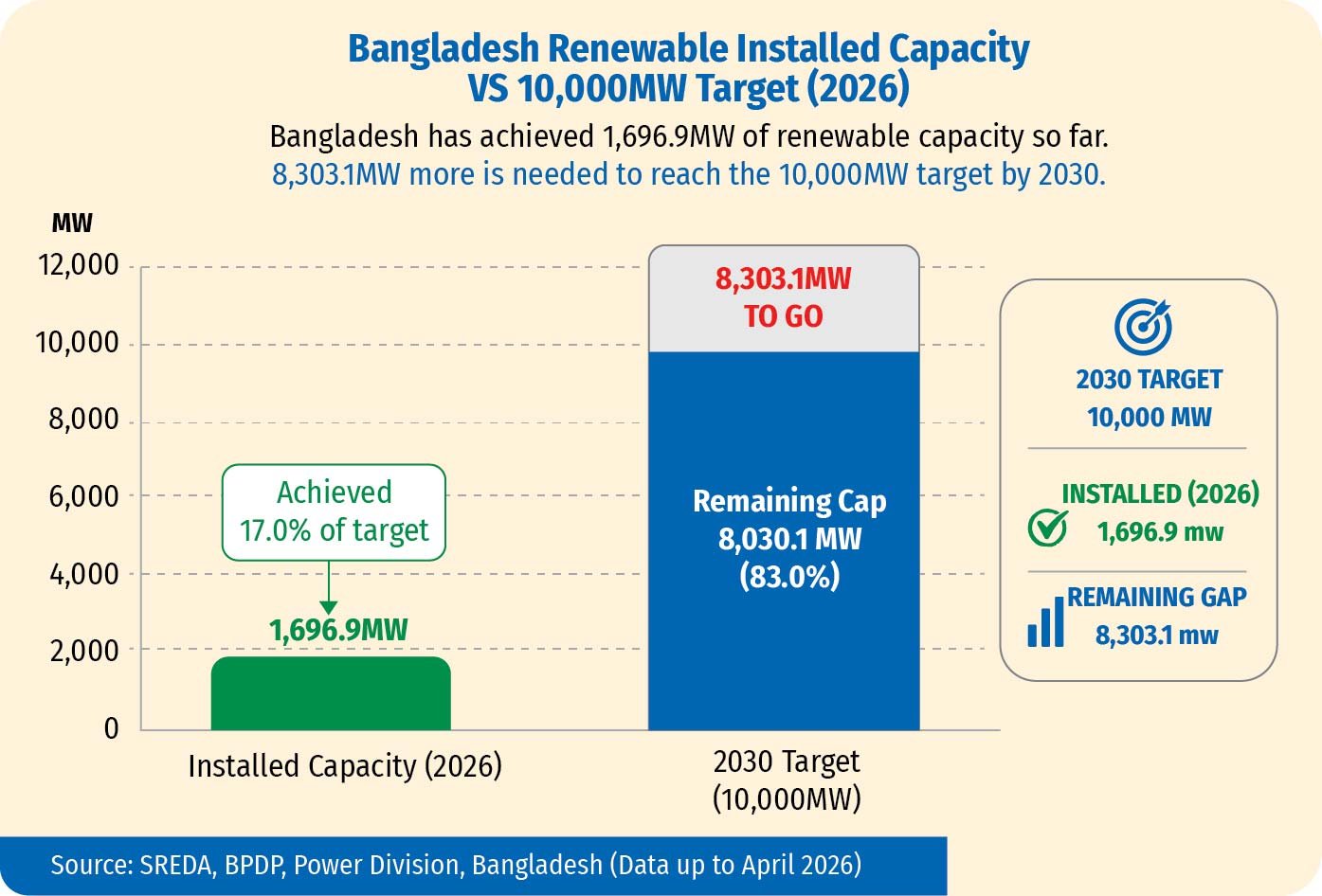

Bangladesh has made renewable progress, but not a renewable transformation. The country gained international recognition for solar home systems that expanded off-grid energy access. Rooftop solar has gradually grown under net metering rules. Some utility-scale solar plants have been commissioned. Pilot wind initiatives have emerged. Waste-to-energy discussions continue. Yet compared with total national electricity demand, renewable capacity remains modest.

This means Bangladesh must now move from pilot-scale renewable policy to mass-scale renewable execution. If the effective renewable base remains limited relative to the 10,000 MW target, then the country may need to add approximately 8,000 to 9,000 MW of new renewable capacity within less than five years.

That is ambitious by any measure. But ambition alone is not the problem. Delivery speed is the problem. Many countries have achieved rapid scaling when the policy environment was right. The question is not a physical possibility. It is institutional readiness.

Is the target realistic?

Yes, but not under business-as-usual conditions. Bangladesh has repeatedly shown that when infrastructure becomes a national priority, projects can move. Major bridges, roads, ports, and generation assets demonstrate that state capacity exists when political commitment aligns with administration. So, the issue is not whether Bangladesh can build things. The issue is whether renewable deployment will receive the same seriousness as given to conventional power expansion.

The target becomes realistic if:

- approvals become time-bound

- land is prepared in advance

- payment security reassures investors

- grid expansion runs in parallel

- rooftop solar scales quickly

- financing channels are mobilized

- institutions coordinate effectively

The target becomes unrealistic if:

- files move slowly

- land disputes stall projects

- utilities delay payments

- transmission lags behind generation

- policy signals remain mixed

- 2026 and 2027 are wasted

In short, 10,000 MW is a governance challenge disguised as an energy target.

Where can the 10,000 MW come from?

A diversified pathway is more realistic than dependence on one technology.

.jpg)

This portfolio spreads risk using different land types and broadens participation.

Rooftop solar may be the fastest route

If speed matters, rooftops matter. Large utility projects often require land acquisition, environmental clearance, relocation concerns, and long transmission links. Rooftop systems avoid many of these barriers. Bangladesh has significant unused roof space across:

- garment factories

- warehouses

- universities

- hospitals

- shopping complexes

- apartment towers

- public offices

- airports

- railway stations

If net metering becomes simpler, approvals digital, and financing accessible, rooftop solar can scale rapidly. For export industries, rooftop systems offer another advantage. International buyers increasingly prefer lower-carbon supply chains. Renewable sourcing can improve commercial positioning. Rooftop solar should therefore be treated not as a side policy, but as an industrial competitiveness strategy.

Rooftops alone cannot deliver 10,000 MW. Bangladesh still needs large projects capable of supplying bulk power at a relatively low unit cost. The challenge is land.

A practical land strategy should prioritize:

- low-productivity land where feasible

- brownfield industrial areas

- reclaimed land after technical review

- reservoir-adjacent zones

- dual-use models combining agriculture and solar where viable

The debate should not become food versus energy. It should become efficient land use rather than poor land planning.

Floating solar deserves serious consideration

Land scarcity makes floating solar strategically attractive. Bangladesh has reservoirs, ponds, and water facilities where appropriately designed projects may be viable.

Benefits include:

- reduced land conflict

- faster deployment in selected sites

- diversification of project geography

- useful supplemental capacity

Floating solar will not replace ground-mounted solar, but it can complement it meaningfully.

Wind: selective but useful

Bangladesh is unlikely to become a wind giant. But that does not mean wind has no role. Selected coastal corridors may support viable projects. Even moderate wind additions can help diversify output patterns and complement solar generation. Wind should be pursued pragmatically, where economics justify it.

The grid challenge nobody can ignore

Many countries discovered that renewable bottlenecks are often transmission bottlenecks. Generation projects receive attention, but substations, evacuation lines, dispatch software, and forecasting systems determine whether renewable power can actually be used efficiently. Bangladesh must therefore treat grid modernization as equal in importance to generation procurement. Necessary priorities include:

- renewable transmission corridors

- modern substations near solar zones

- improved load forecasting

- flexible dispatch systems

- digital monitoring tools

Without this, new capacity may be underutilized.

Storage and system flexibility

A common criticism of renewables is intermittency. Solar output varies by time of day. Wind output varies by weather. This concern is real but manageable. Modern power systems use combinations of:

- battery storage

- demand response

- flexible gas peakers

- diversified geography

- stronger transmission networks

- forecasting technology

Bangladesh does not need 100 percent renewable power by 2030. It needs a smarter mixed system with a larger renewable share. That is a planning challenge, not a reason for paralysis.

Financing the transition

Even when renewable power is cost-effective over time, upfront capital is substantial. That means financing structure matters enormously. Bangladesh should actively pursue:

1. Green bonds―Domestic or sovereign green bonds can channel capital into bankable projects.

2. Concessional climate finance―Development partners are increasingly willing to support clean infrastructure.

3. Blended finance―Public risk-sharing can unlock private investment.

4. Local bank participation―Domestic banks should treat renewables as productive infrastructure, not niche lending.

5. Currency risk mitigation―Foreign investors need comfort on exchange-rate exposure.

If financing costs remain too high, even cheap technologies become expensive.

What the government must do in 2026–27

These two years will determine whether the target remains alive.

Step 1: Publish annual milestones―Do not manage only toward 2030. Publish yearly targets.

Step 2: Launch competitive auctions―Ready projects should enter transparent bidding immediately.

Step 3: Reform rooftop net metering―Applications should be digital, simple, and time-bound.

Step 4: Solarize public assets―Schools, hospitals, ministries, stations, and airports should become visible early adopters.

Step 5: Create a renewable land bank―Pre-cleared sites can save years.

Step 6: Build skills pipelines―Technicians, EPC firms, and engineers must scale with demand.

Step 7: Publish monthly dashboards―Show MW awarded, under construction, and commissioned. Transparency creates pressure. Pressure improves delivery.

What can Bangladesh learn from others?

India demonstratedthat competitive auctions reduced solar tariffs dramatically when scale and policy confidence aligned.

Vietnam showed thatstrong incentives rapidly unlocked rooftop growth, though later policy correction was needed.

Pakistan’s recent distributed solar growth suggests consumers move quickly when economics are favorable.

Bangladesh does not need to copy any particular model. But it should be learned selectively and pragmatically.

What happens if Bangladesh fails?

Failure would carry costs beyond embarrassment. It would likely mean:

- continued import dependence

- higher long-run tariffs

- repeated subsidy pressure

- missed green investment flows

- slower industrial decarbonization

- weaker competitiveness for exporters

- delayed energy security

In other words, failure would preserve yesterday’s risks.

What happens if Bangladesh succeeds?

Success would not mean perfection. But it would mean a structural turning point. Bangladesh would gain:

- a more diversified power system

- lower fuel vulnerability

- stronger investor confidence

- greener export branding

- new domestic industries and jobs

- better long-run affordability prospects

Most importantly, success would prove that Bangladesh can execute a modern energy transition at scale.

The political economy nobody likes to discuss

Every energy transition creates winners and losers. Renewables may challenge interests linked to:

- imported fuel supply chains

- legacy procurement models

- slow approval cultures

- institutional inertia

That is why leadership matters.

The transition should be framed not as ideology, but as:

- lower long-run electricity cost

- lower import dependence

- stronger reserves

- cleaner cities

- better jobs

- stronger export competitiveness

When framed economically, resistance weakens.

Final verdict: dream or deliverable?

The 10,000 MW target is not a night dream. But it is also not self-executing. Bangladesh still has enough time—but not enough time to waste. As of early 2026, a realistic scorecard says the following real picture:

Political ambition: High

Technical feasibility: Moderate to high

Institutional readiness: Moderate

Financing potential: High if structured well

Probability under business-as-usual: Low to moderate

Probability with urgent reforms: Strongly achievable

If 2026 becomes the year of land mobilization, auction launches, rooftop acceleration, grid investment, financing reform, and monthly accountability, then 2030 can mark the beginning of a more secure and modern energy era.

If 2026 becomes another year of speeches, committees, and delayed files, the target will quietly age into irrelevance. The next chapter of Bangladesh’s power story will not be written by targets alone. It will be written by turbines, panels, substations, batteries, and the discipline to deliver them. The countdown has already begun!!!!!

DR. Shahi Md. Tanvir Alam, Visiting Researcher, RIS MSR 2021+ Project, School of Business Administration in Karviná, Silesian University in Opava, Czechia, Email: tanvir@opf.slu.cz /shahi.tanvir@gmail.com

Download Cover Article as PDF/userfiles/EP_23_23_Cover_Article.pdf