Continued war and conflict across the Arab and Persian Gulf region have triggered major supply chain disruptions and sharp increases in primary fuel prices. This region remains the world’s largest producer and exporter of crude oil, petroleum products, and liquefied natural gas (LNG). Around 20% of global primary fuel trade passes through the Strait of Hormuz, which has effectively been choked due to the conflict.

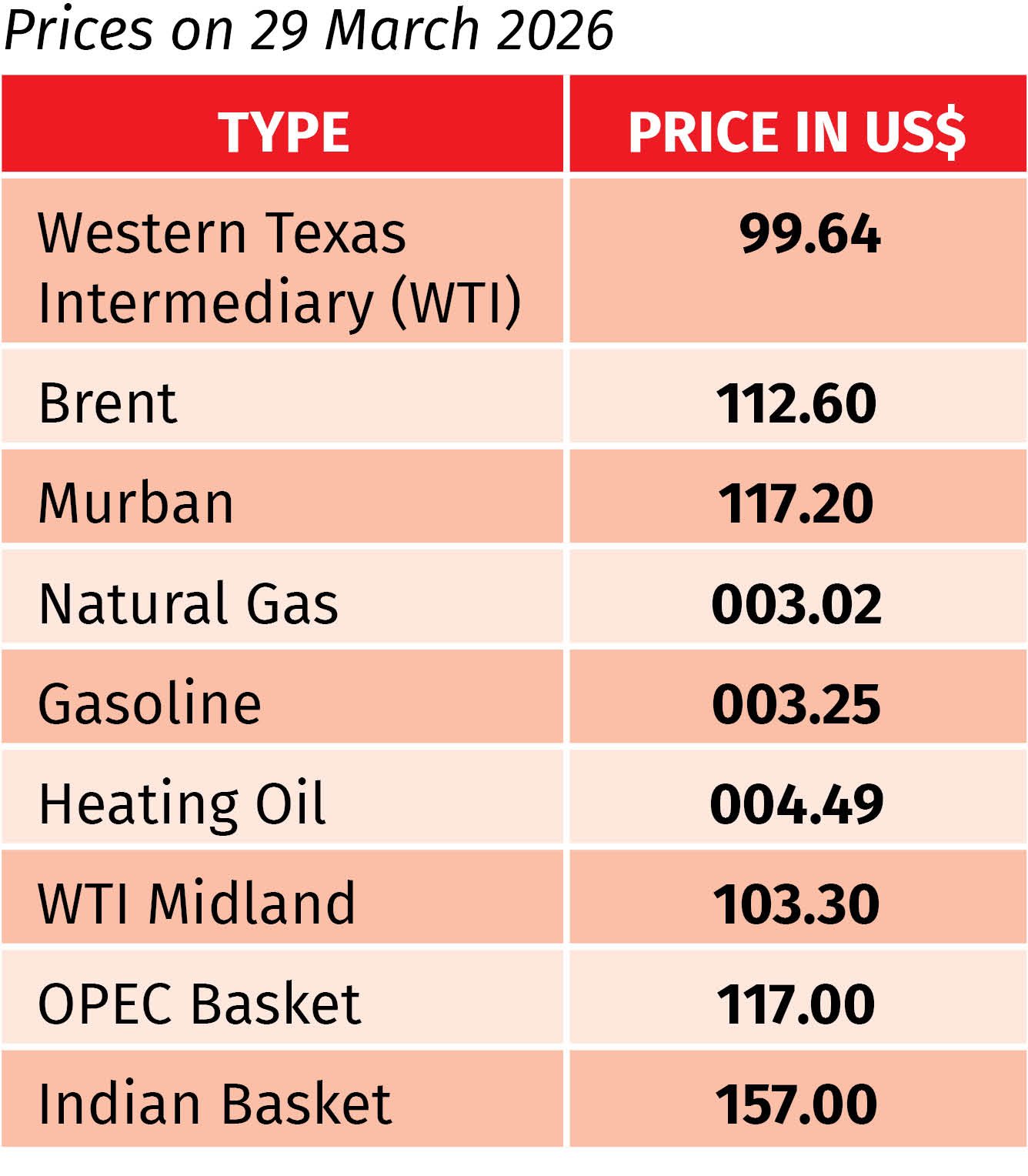

The war has also affected key energy infrastructure, including the South Pars gas field, the LNG hub at Ras Laffan, and oil installations in Bahrain, the UAE, Kuwait, and Saudi Arabia. Brent crude prices have surged past $110 per barrel. At the same time, the warring parties have threatened further attacks on energy, power, and water infrastructure. The disruption of shipping through the Strait of Hormuz has severely affected the transportation of fuel, fertilizer, and other essential commodities.

As a result, both energy and food security have become increasingly uncertain for import-dependent countries. Nations across South and Southeast Asia, including Bangladesh, have begun implementing contingency measures to cope with the crisis. However, panic buying by consumers and internal supply chain disruptions have worsened the situation in Bangladesh. Long queues at petrol stations have become common, with many consumers returning empty-handed as pumps run out of stock. Several stations have reported limited or irregular fuel supply from depots.

Government ministers and officials have repeatedly assured the public that adequate reserves are available and have urged restraint and conservation. However, these reassurances have had limited impact. Authorities have intensified monitoring across the supply chain, and some unscrupulous actors have been arrested. Pump owners, meanwhile, point to irregular depot supply during weekends and holidays, combined with a sudden surge in demand, as key drivers of the crisis.

Supply Chain Disruptions Deepen Crisis

Countries dependent on imported fuel have faced severe challenges since the outbreak of the conflict. The situation escalated after the United States and Israel reportedly targeted Iran’s energy hub at Kharg Island and facilities in the South Pars gas field. Iran retaliated with missile strikes on petroleum and LNG infrastructure in Qatar, Saudi Arabia, the UAE, Bahrain, and Kuwait. As a result, production capacity across these facilities has been partially disrupted, driving up global prices of crude oil, refined products, and LNG.

Iran’s move to regulate fuel and commodity transport through the Strait of Hormuz has further disrupted global supply chains. For countries like Bangladesh, the impact has been compounded by internal logistical challenges. With limited strategic reserves, Bangladesh has been forced to introduce fuel rationing measures.

The country’s lack of a deep-sea port adds another layer of complexity. Crude oil and coal must be transported via lighter vessels after being offloaded from larger ships offshore. Ensuring adequate fuel supply for these lighter vessels has become increasingly difficult, further straining the supply chain.

Fuel rationing was introduced before the government could fully stabilize internal supply chain management, which contributed to panic buying. Opportunistic market players have also attempted to exploit the situation. While supplies of octane, petrol, and LNG remain relatively stable, the main concern lies with crude oil and diesel.

Some countries have already introduced measures such as remote work policies and vehicle restrictions based on license plate numbers. Bangladesh must now adopt pragmatic, transparent, and well-coordinated policies to manage both supply and demand effectively and prevent the crisis from deepening further.

Iran initially announced that it would allow vessels carrying fuel for six friendly countries to pass through the Strait of Hormuz for a limited period. However, after a Pakistan-flagged ship transporting fuel for the United States reportedly attempted to transit the route, the decision was reversed, and the strait was effectively closed again. There have been indications of possible dialogue between Iran and the United States, reportedly brokered by Pakistan, but a meaningful truce appears unlikely at this stage. Instead, fresh threats have emerged of further attacks on fuel, power, and water infrastructure.

With limited options, Bangladesh has begun sourcing liquid fuel and LNG from alternative suppliers in the spot market, significantly increasing subsidy requirements. The new government is currently in no position to raise fuel or electricity prices due to concerns over inflation. Even adjustments to jet fuel prices could affect air travel. However, it remains uncertain how long Bangladesh can continue to absorb these costs through subsidies. Sooner or later, fuel and electricity prices may need to be adjusted, which would likely trigger a broader increase in commodity prices and fuel inflationary pressures.

Conclusion

The conflict shows no immediate signs of ending. Access to fuel resources from the Arab and Gulf regions may remain constrained for an extended period. Bangladesh must therefore diversify its energy import sources and secure the financial capacity to procure fuel at higher prices. At the same time, it needs to manage its internal fuel supply chain more efficiently.

Jobs in the power and energy sector should be declared essential services to ensure uninterrupted operations. The domestic fuel supply chain must remain smooth and continuous, without disruptions due to holidays or logistical gaps. Strong administrative oversight is also necessary to prevent irregularities.

Equally important is public cooperation. Consumers must be encouraged to use fuel and electricity more responsibly. At the same time, the government must accelerate efforts to explore and develop domestic energy resources, alongside expanding renewable energy initiatives on a war footing. Managing the period from April to November 2026 will be a critical test for the country’s energy security and economic stability.

Download Special Report As PDF/userfiles/Special Report.jpg

{kind=link}