It is well understood that Bangladesh’s uncertain energy security has severely impacted both foreign direct investment (FDI) and domestic investment. Chronic gas shortages mean a large portion of gas-based power plants cannot operate for most of the year. Only two of the seven state-owned fertilizer plants remain functional. Many small and medium industries have shut down, while most large industries are struggling to keep operations running.

This crisis is largely the result of the absence of a long-term strategic plan, poor coordination among key stakeholders, the neglect of skilled professionals in the energy and power sectors, and a heavily politicized and corruption-prone management system. Over the past year, the interim government has failed to grasp the full scope and complexity of the crisis. While some of their actions have brought marginal improvements, they have not addressed the root causes. As a result, the energy and power sectors continue to function in a “business-as-usual” mode.

A newly elected democratic government is expected to take office in early 2026. For it, the energy and power sectors must be among the highest priorities. Bangladesh urgently needs a reliable and uninterrupted supply of electricity and gas to drive economic growth. Without consistent, transparent policies, sustained inflows of both foreign and local investment will remain elusive. If the current energy crisis continues, the country will face worsening unemployment and dwindling export earnings. There are no magical solutions—only sound strategies and vision. Let us hope the political leadership has both.

Present Situation of Power and Energy Supply Chain

Over the past 25 years, Bangladesh’s power and energy sector has expanded significantly, but this growth did not follow an integrated and comprehensive master plan. Although the government developed two Power System Master Plans (PSMP 2010 and 2018) with JICA’s support, and more recently the Integrated Energy and Power Master Plan (IEPMP 2023), none of these plans were seriously implemented. Inadequate data and flawed assumptions further weakened the planning process.

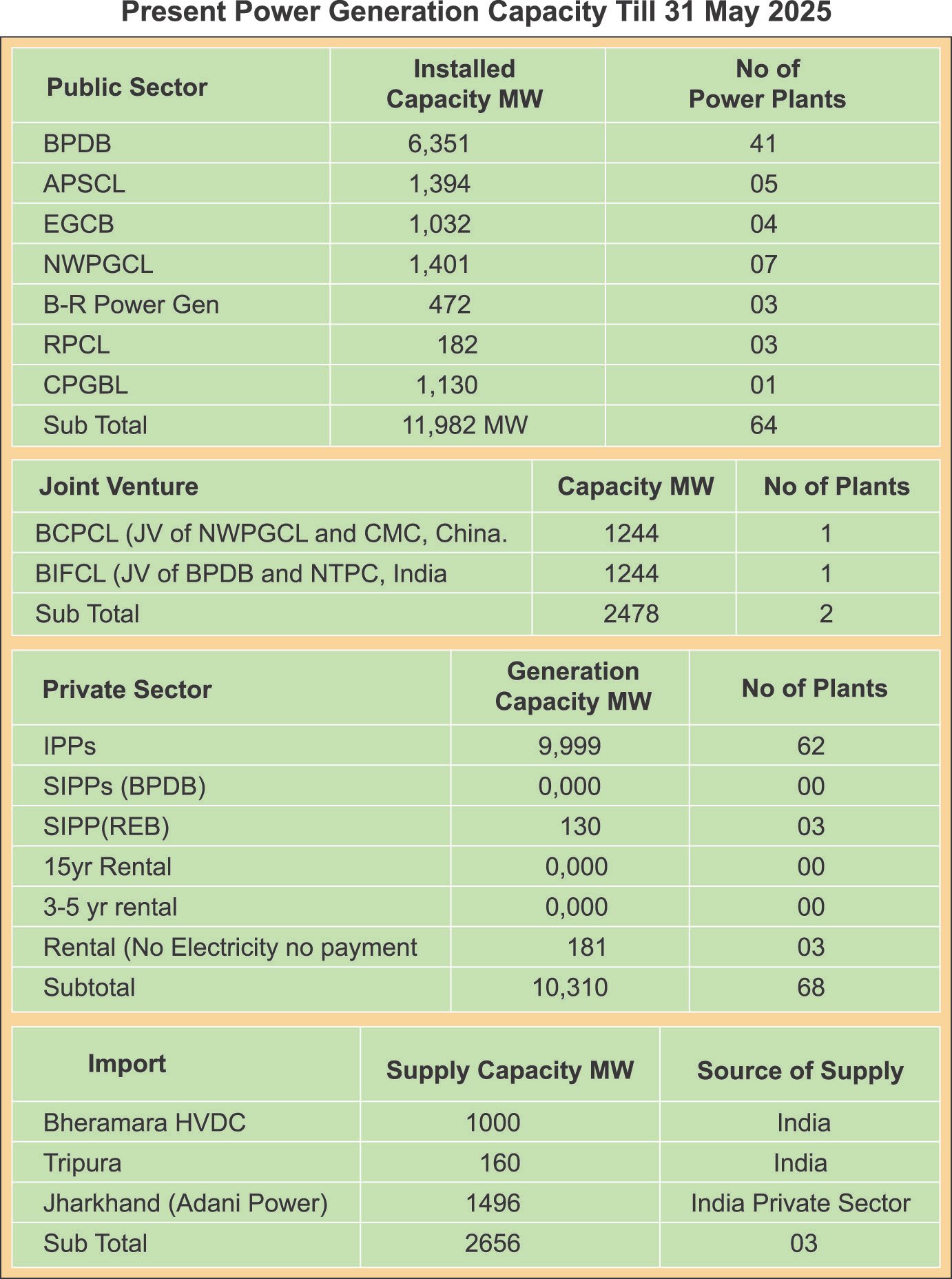

As a result, the power supply chain continues to suffer from a lack of primary fuel. Bangladesh has depleted most of its natural gas reserves—a mono-fuel resource. It also faces constraints in importing alternative fuels like coal, LNG, and liquid fuels. This failure is evident in the sector’s inability to consistently generate even 16,000 MW of electricity, despite having an installed generation capacity of 30,780 MW (including grid and non-grid sources). Meanwhile, superior-quality domestic coal lies untapped, significant onshore and offshore petroleum reserves remain unexplored, and renewable energy potential remains neglected.

The public sector power plants account for 44% of the total generation capacity. Power plants in many areas like Ghorashal, Shiddhirganj, and Sirajganj suffer from poor gas supply. However, some of the ageing plants are fuel-inefficient and should be retired or modernized.

The above two plants are based on imported coal and are located at Payera Patuakhali and Rampal, Bagerhat. They suffer from the dollar crisis and coal transportation challenges. Rampal Power plants also suffered from frequent technical constraints. The challenges of coal transportation added to the cost of generation. For both the plants coal needs to be transported in half filled coal carriers increasing the cost of generation.

The private sector has the capacity to contribute 37% to the total generation now. Some of the plants recently installed at Meghnaghat are highly fuel efficient. But there are issues of gas supply both from supply constraints and gas transmission issues.

Imports can contribute 10% of the total capacity. Interim government could manage to clear outstanding dues of Adani Group. Import remains a bit of concern for BPDB responsibilities of payment on time.Total Installed Capacity of Grid Power: 27,426 MW. Adding 2800 MW Captive, Renewable and Off grid HFO = 30,780 MW.

The 2800 MW capacity of captive generation figure differs with information received from the BERC. This needs to be checked and verified. All impediments for supplying power to industries grid power must be resolved, enabling saving of some gas now being used in captive generation.

.jpg)

The Bangladesh Power Development Board (BPDB) requires about 2,100 MMCFD of gas to operate all gas-based power plants. However, the current gas production and distribution infrastructure can supply no more than 1,200 MMCFD—even during peak summer months. This shortfall forces the use of furnace oil-based peaking plants, which are costlier. BPDB also struggles to make payments to independent power producers (IPPs), many of whom receive capacity payments under their contracts. The dwindling supply of proven gas reserves makes it increasingly difficult for Petrobangla to meet the needs of the power sector, fertilizer plants, and industries. The current administration must urgently revisit the national fuel mix, giving top priority to long-term sustainability.

Recommendations

The current government must make strategic decisions to mine domestic coal. All feasible options for boosting gas production from onshore and offshore fields should be pursued. Simultaneously, the barriers to increasing the share of renewable energy must be addressed. Bangladesh is under no international obligation to reduce emissions and faces no embargo on using its own fossil fuels.

Given the country’s geographical limitations and current geopolitical conditions, Bangladesh cannot ensure long-term energy security as a net energy importer. It has already suffered from price shocks and supply disruptions. Until 2040, Bangladesh could feasibly maintain a 75:25 fuel mix between domestic and imported fuels—provided it develops sound, realistic plans and executes them with professionalism.

The stranded gas reserves in Bhola must be urgently connected to the national grid. Within six months of assuming office, the new government must engage a reputable international EPC contractor to construct a gas transmission pipeline from Bhola to the national grid in Khulna. This is a technically complex task, well beyond the capacity of local contractors. If initiated by end-2026, the pipeline could be commissioned by early 2029.

An accredited reservoir specialist company should also be engaged to accurately assess Bhola’s gas reserves. Establishing this infrastructure would encourage international oil companies (IOCs) to invest in petroleum exploration across the southern region. Supplying gas to greater Barishal and Khulna could trigger an industrial transformation across southern Bangladesh.

Other gas prospects such as Chattak and Tengratilla should be developed on a priority basis. With the dispute with NIKO reportedly resolved, pending formalities must be completed swiftly so that BAPEX can resume operations. Furthermore, strategic partners should be engaged to help BAPEX explore gas-rich areas in the Chittagong Hill Tracts, including Joldi, Kasalang, Sitapahar, and Patiya. Deeper layers of existing gas fields also present untapped potential and should be assessed for commercial viability.

Petrobangla and the Energy and Mineral Resources Division (EMRD) must also proactively negotiate Chevron’s proposal to explore Blocks 12 and 13. Chevron already operates the Bibiyana, Jalalabad, and Moulvibazar gas fields, and is familiar with the technical challenges in Bangladesh. A win-win contract could be mutually beneficial.

We also hope the interim government will finalize the new bidding round for offshore production-sharing contracts (PSCs) and complete the onshore bidding process. The incoming government must prioritize this. By 2027, at least 10 drilling rigs should be operational across onshore and offshore sites. If this is achieved, Bangladesh’s energy portfolio could look significantly better by 2030.

LNG import strategy also needs re-evaluation. The interim government misjudged the cancellation of the third FSRU (Floating Storage Regasification Unit) contract, which had been negotiated under a special act. Over the past year, it failed to engage a contractor or even issue a tender. The matter is now in court, but it would be advisable to resolve the dispute outside of litigation, if possible.

Similarly, the blanket cancellation of letters of intent (LOIs) for grid-connected solar projects was a misstep. Each case should have been reviewed individually. It is unlikely the interim government can resolve these issues before leaving office. The incoming administration must assess all challenges in the energy transition and build institutional capacity to scale up renewable and clean energy.

Conclusion

The following can be recommended in order of merit:

- Professionally review the IEPMP with the help of Bangladeshi experts to develop a rational, integrated energy and power system master plan.

- Decide on mining domestic coal, preferably for use in power generation and industry.

- Immediately evacuate stranded gas from Bhola and integrate it into the national grid.

- Prioritize development of Chattak and Tengratilla gas fields.

- Select and engage a strategic partner for BAPEX to explore gas prospects in the Chittagong Hill Tracts and deepen exploration of existing fields.

- Do not delay PSC bidding for both offshore and onshore exploration.

- Take pragmatic steps to advance FSRU and land-based LNG terminals.

To achieve all this, Petrobangla and its affiliated organizations must prioritize human capital—appointing qualified, experienced professionals to the right roles. In short, a paradigm shift in management and execution is imperative if Bangladesh is to overcome its energy crisis.

Download Special Article As PDF/userfiles/EP_23_3_Special_Article.pdf